Stepping Back to Observe Is Preferable to Rash Responses

Advice: "Use the Adjustment as an Opportunity to Increase Weight"

[Asia Economy Reporter Lee Seon-ae] "February calls for the attitude of 견토방구 (見兎放狗), meaning a bit of patience can increase the chances of a successful hunt." Kim Hyung-ryeol, Head of Research Center at Kyobo Securities, likened the February stock investment strategy to the four-character idiom that suggests it is okay to spot a rabbit and send a hunting dog, emphasizing "there is no need to be too hasty" and "what is needed now is breath control." He explained, "Since the stock market experienced extreme stagnation last year, the January rally was even more welcome, but it has become more difficult to establish strategies and scenarios for February," adding, "It is a challenging situation to decide whether to continue the current momentum as is or to manage risks in anticipation that the rebound of asset prices, which have advanced too far, may face resistance again."

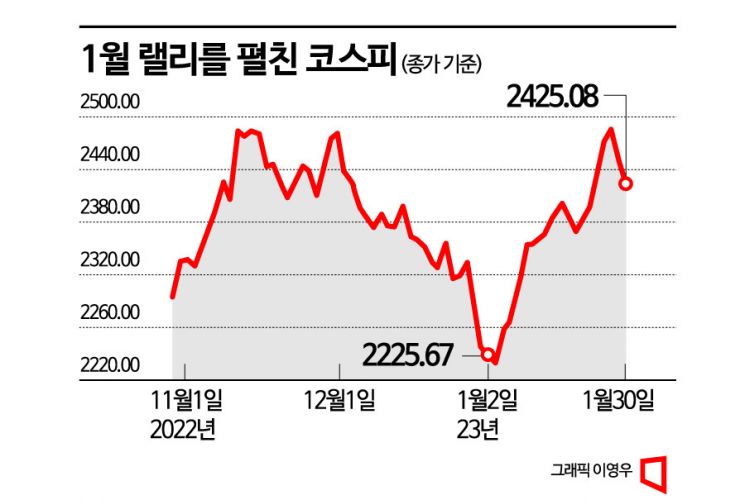

The outlook on the domestic stock market in February shows coexistence of 'optimism' and 'pessimism' among securities firms. The KOSPI, which broke the initial forecast that there would be no January effect and rallied from the start of the new year, recently slipped for two consecutive trading days, ultimately failing to surpass 2500. There are forecasts that a major correction may occur in February.

On the other hand, there is a positive view that the rally, somewhat weakened due to the strong market momentum, will continue with an upward trajectory. Amid these conflicting forecasts, the common consensus is a volatile market. As Kim emphasized, the dominant investment advice is to approach with a cautious, observant stance rather than premature action.

According to the Korea Exchange, on January 31, the last trading day of January, the KOSPI closed at 2425.08, down 1.04% (25.39 points) from the previous trading day. Despite the January rally, it failed to surpass the 2500 mark and slid to 2420 by the end of the month. On January 30, after five consecutive days of gains, the market closed at 2450.47, down 1.35% (33.55 points) from the previous day. This was the first time in about a month since December 29 last year that the KOSPI fell more than 1% in a day.

Accordingly, pessimistic views on the February stock market are gaining traction. With the January rally reflecting expectations, the market is judged to enter a correction phase with volatility rather than further gains. The pessimistic view holds that in January, excessive market optimism about easing tightening led to confirmation bias, reflecting only positive news. There is even caution that if the U.S. Federal Reserve (Fed) implements stronger monetary policies, the market could face a greater shock.

Lee Kyung-min, a researcher at Daishin Securities, said, "Since the beginning of the year, the market has amplified expectations based on small changes, and recently this process has been expanding and reproducing," diagnosing, "The market is dominated by confirmation bias investment sentiment that overreacts to small good news and ignores the darker realities." He added, "If excessive expectations for rate cuts persist, the Fed may try to erase even dovish tones beyond hawkish remarks to alert the market." He predicted that the domestic stock market will undergo a significant correction around the Federal Open Market Committee (FOMC) meeting. He emphasized, "It is necessary to consider whether there will be 'surprise momentum' exceeding current market expectations while confirming China's economic recovery speed, U.S. monetary policy stance, and Korean semiconductor industry outlook. If expectations are met, the stock market will stagnate, but if 'surprise momentum' is absent or even small disappointments arise, global stock markets could be greatly shaken, so downside risks must be guarded against."

Ahn Young-jin, a researcher at SK Securities, also said, "The FOMC's baby step (0.25 percentage point rate hike) could strengthen the signal to pause rate hikes, but Chairman Jerome Powell will try not to give too dovish a tone," adding, "There may be a need to reduce stock exposure."

There is also a forecast that the last low point of the year will come in February. Park Seung-young, a researcher at Hanwha Investment & Securities, said, "The January stock market rebound started from expectations that the rate hike pace would slow at the February FOMC, but February will begin with the fading of those expectations," adding, "The pivot expectation has already been priced into the market, and if the stock market corrects in February, it could be the last low point of the year."

Even if it is not a 'confirmation of the bottom,' there is a view that the market will technically hit resistance in February. Although the distance to the previous rally high of 2500 has narrowed, considering the recent decline in trading volume, technical resistance may be encountered. Choi Yoo-jun, a researcher at Shinhan Investment Corp., said, "Ultimately, corporate earnings constrain the upper limit of the stock market," adding, "In past rebound phases, the direction of earnings was important, but current earnings estimates continue to be revised downward."

While it is undeniable that the market is currently in an overbought phase, there is also a positive view that it will trend upward. Kim Dae-jun, a researcher at Korea Investment & Securities, said, "The KOSPI is currently in an overbought phase and the upward momentum is gradually weakening," but added, "However, the decline in market interest rates is favorable for the stock market, so in the long term, the KOSPI will trend upward." Jung Myung-ji, head of investment information at Samsung Securities, said, "It is difficult to interpret the rise driven by foreign demand as overheating," adding, "Currently, it is a recession, so earnings are deteriorating, but the positive atmosphere of possible rate cuts creates a 'liquidity-driven market,' so it is normal for earnings and stock prices to diverge," forecasting the upward trend to continue.

Kim Hyung-ryeol expects the stock market to rebound around the second quarter after February. He analyzed, "Given the stock market's characteristic of leading the economy, the bottom of economic sentiment is expected to soon become apparent," adding, "Considering that the economic sentiment index has been declining for 13 months so far, even if it breaks the longest record, a rebound attempt in the stock market could appear in the second or third quarter." Past periods of economic sentiment decline recorded 17 months during the IT bubble, 14 months during the global financial crisis, and 16 months during the U.S.-China trade war.

As analyses suggest that the earnings estimate decline phase is entering its final stage, there is investment advice to maintain a watchful stance while using volatility as an opportunity to increase exposure. Jung In-ji, a researcher at Yuanta Securities, said, "The medium-term lows of global major stock markets including the KOSPI are rising, so even if short-term gains are limited, the long-term trend is favorable for gains," advising, "A strategy to find buying opportunities during short-term corrections is valid." Roh Dong-gil, head of domestic equity strategy at Shinhan Investment Corp., analyzed, "The earnings estimate decline, which has approached the drop from previous highs experienced during past recessions, is likely to end in the first quarter," adding, "From a mid- to long-term perspective, a selective, concentrated portfolio is necessary as it can influence estimate forecasts."

Kim Yu-mi, a researcher at Kiwoom Securities, said, "The February stock market is expected to enter a phase where expectations materialize, with volatility continuing until mid-month," recommending, "There may be a price pullback in growth and large-cap stocks that rebounded strongly in January, and for risk management, it is advisable to focus on mid-to-large caps and sectors such as healthcare and capital goods."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}