Rising Interest Rates Cause Psychological Contraction and Financial Burden

More Than Half of New Loans at High Interest Rates

"The interest rate on unsecured loans is 7%, which is psychologically very discouraging. I borrowed 50 million won from my main bank, and the monthly interest is 300,000 won. From now on, even if I get 100,000 won, I plan to pay off the loan first without spending it elsewhere." (Office worker Lee Min-jeong (31))

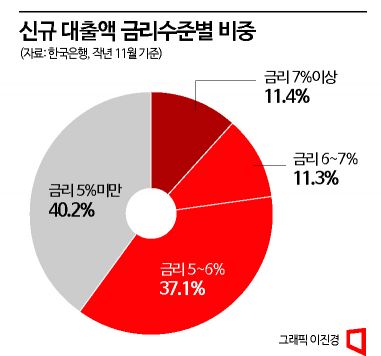

It has been revealed that half of the new household loans issued by deposit banks in South Korea are concentrated in the 5-7% interest rate range. According to the Bank of Korea Economic Statistics System on the 6th, as of November last year, loans with interest rates between 5% and 7% accounted for 48.4% of new loans issued by deposit banks. This is the highest level in about 11 years since February 2012 (52.7%). New loans with high interest rates above 7% accounted for 11.4% of the total.

An official from a commercial bank said, "Since the beginning of the new year, the upper limit of mortgage loan interest rates at the five major banks has exceeded 8%, and unsecured loan interest rates are also approaching 8%. If the Bank of Korea raises the base rate again on the 13th of this month, interest rates are expected to rise further."

"Is there any cheaper loan available?"

As the interest burden grows, there is also a movement to switch to loans with cheaper interest rates. For those who have taken out mortgage loans, there is high interest in the special Bogeumjari Loan that the financial authorities will introduce in the first quarter. This loan has no income requirements and can be used for home purchase or living stabilization funds. Even if the annual salary is high, if the house price is under 900 million won, loans up to 500 million won with interest rates in the 4% range are possible.

Also, more financial consumers are refinancing their mortgage loans from commercial banks to internet banks with lower interest rates in the 4% range. According to KakaoBank, the amount of mortgage loans refinanced from other banks to KakaoBank (based on contract amount) reached 95.3 billion won as of the end of October last year. It was 6.3 billion won at the end of March last year, meaning it increased 15 times in about half a year.

As the U.S. central bank, the Federal Reserve (Fed), hinted at additional interest rate hikes, attention is increasing on whether the Bank of Korea's Monetary Policy Committee will raise rates at its meeting scheduled for the 25th. The photo shows a loan counter at a commercial bank in downtown Seoul on the 19th. Photo by Hyunmin Kim kimhyun81@

As the U.S. central bank, the Federal Reserve (Fed), hinted at additional interest rate hikes, attention is increasing on whether the Bank of Korea's Monetary Policy Committee will raise rates at its meeting scheduled for the 25th. The photo shows a loan counter at a commercial bank in downtown Seoul on the 19th. Photo by Hyunmin Kim kimhyun81@

Only Middle-Income Groups Increase Loan Balances

As interest rates rise, the ability to respond to loans differs according to income levels. Low-income groups have reduced loan balances because they cannot borrow money, and high-income groups have decreased loan balances by repaying loans to reduce interest burdens. The average loan balance increased only for the middle-income groups.

According to a report titled "Changes in Borrowers' Repayment Ability by Income Level Due to Interest Rate Increases and Implications" released by the Korea Institute of Finance at the end of last month, the average loan balance of low-income borrowers (income first quintile) decreased by 3.64 million won (8.8%) from 41.34 million won in September 2021 to 37.7 million won in September 2022. This is because as market interest rates rose, secondary financial institutions could no longer raise interest rates due to the legal maximum interest rate ceiling and stopped lending, pushing low-income groups into a loan cliff.

High-income groups (income fifth quintile) saw their average loan balance decrease by 0.5%, from 152.76 million won to 152 million won during the same period. The average loan balances of middle-income groups (income second, third, and fourth quintiles) increased by 3.2% (1.46 million won), 4.9% (2.72 million won), and 4.1% (3.28 million won), respectively, compared to a year ago. The report analyzed, "Unlike high-income groups who have the capacity to repay and have responded to increased interest burdens due to rising rates, middle-income groups are experiencing increased repayment burdens due to the interest rate hikes."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}