China Competition Authority Approves Corporate Merger

M&A Impact Uncertain Amid National Protectionism

LCC Industry's Opportunity to Enter China Increases

China's competition authorities have approved the corporate merger of Korean Air and Asiana Airlines, signaling a green light for the merger. However, there are concerns that the effects of the merger and acquisition (M&A) may be lower than expected due to the protectionist policies of each country for their domestic companies.

China's competition authorities have approved the corporate merger of Korean Air and Asiana Airlines, signaling a green light for the merger. However, there are concerns that the effects of the merger and acquisition (M&A) may be lower than expected due to the protectionist policies of each country for their domestic companies. [Image source=Yonhap News]

[Asia Economy Reporter Oh Gyumin] China's competition authorities have approved the corporate merger between Korean Air and Asiana Airlines, signaling a green light for the merger. However, there are concerns that the effects of the merger and acquisition (M&A) may be lower than expected due to each country's policy of protecting their domestic companies.

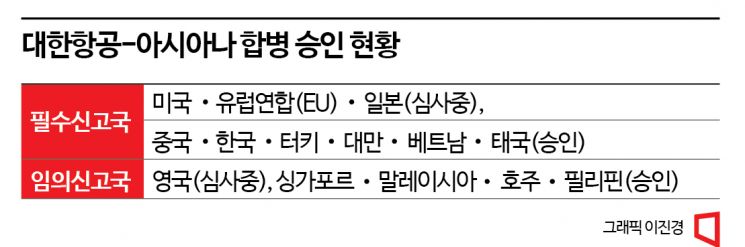

On the 26th, Korean Air obtained corporate merger approval related to the acquisition of Asiana Airlines from China's competition authorities, a mandatory reporting country. This is the first mandatory reporting country approval since receiving conditional approval from the Korea Fair Trade Commission in February this year. For the M&A to proceed, corporate merger approval is required from mandatory reporting countries among the 14 major reporting countries. The merger cannot proceed without approval from even one country. With the approval from China's competition authorities, the countries requiring approval are the United States, the European Union (EU), Japan, and the United Kingdom, which is a voluntary reporting country.

Corrective Measures Such as Slot Allocation... "Strategic Approach Needed in Future Negotiations"

China's State Administration for Market Regulation granted conditional approval to Korean Air. They expressed concerns that the market share of the two companies would increase upon merger, potentially restricting competition. Specifically, for a total of nine routes?five routes that the Korea Fair Trade Commission had judged to have competition restriction concerns plus four additional overlapping routes between the two airlines?a kind of 'restriction' was imposed. If an airline wishes to newly enter these routes, Korean Air must support the necessary slot transfers. A slot is the right for an airline to use airport facilities at a desired time to take off and land aircraft.

The United Kingdom also demanded similar corrective measures from Korean Air. The UK's Competition and Markets Authority (CMA) requested that up to seven slots at London Heathrow Airport be provided to the British airline Virgin Atlantic. Korean Air submitted a corrective plan, which the CMA has in principle accepted, and the approval decision will be made in January next year.

Although Korean Air accepted the corrective measures and received corporate merger approval, there are views that the merger effects may be less than expected. Slots are assets that determine an airline's competitiveness, so transferring slots results in losses. Holding slots during preferred time slots allows airlines to carry more passengers and generate revenue. If slots are given to other airlines, the competitiveness of the original airline decreases.

In particular, a strategic approach is needed when obtaining corporate merger approval targeting the EU, which is a major route for large airlines. Professor Hwang Yong-sik of the Department of Business Administration at Sejong University said, "Korean Air should pay more attention to various conditions, including slot provision, to ensure synergy effects when negotiating with the EU."

LCCs Could Be Beneficiaries... Increased Possibility of Entering Chinese Routes

Meanwhile, if the merger between Korean Air and Asiana Airlines becomes a reality, low-cost carriers (LCCs) specializing in short-haul routes are expected to be the biggest beneficiaries. This is because they could enter the Chinese routes that will be relinquished upon the merger. Previously, China's competition authorities required that, besides the five routes for which the Korea Fair Trade Commission demanded concessions, the Seoul?Beijing, Shanghai, Changsha, and Tianjin routes be conceded to other airlines. These routes are so-called 'prime routes' with high passenger demand.

Jeju Air and T'way Air could apply for new entry on these routes. However, Air Seoul, Jin Air, and Air Busan, which are subsidiaries of Korean Air and Asiana Airlines, are not allowed to newly enter these routes.

Chinese routes account for a large portion of revenue for LCCs, which mainly operate short-haul flights. Jeju Air's revenue from Chinese routes last year was the largest among its international routes. T'way Air's revenue from Chinese routes accounted for 4.6% as of the second quarter this year, ranking second after domestic routes, which accounted for 88.8%.

Following the Chinese government's easing of quarantine policies, LCCs have recently been increasing their Chinese routes to recover demand. T'way Air, operating three routes including Incheon?Wuhan, Shenyang, and Daegu?Yanji, will add the Incheon?Jinan (Jinan) route starting January 13. Jeju Air is also preparing to resume operations on the Yantai route.

Professor Hwang said, "Countries that have approved corporate mergers or accepted corrective measures so far have attached conditions to protect their domestic companies. This atmosphere is expected to continue in the allocation of Chinese route slots, so LCCs should carefully monitor and prepare accordingly."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}