Korean Industry Focused on Finished Products Has Relied on Imports of Materials, Parts, and Equipment

Importance of Parts Suppliers Has Long Been High... Now the 'Parts Era'

Semiconductor Customers, Display Materials, Packaging Portfolio, etc.

[Asia Economy Reporter Moon Chaeseok]

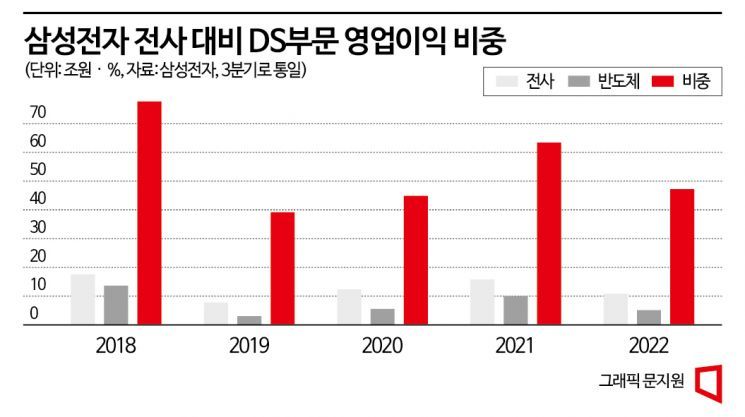

According to Samsung Electronics' reports submitted to the Financial Supervisory Service over the past five years (2018?2022), the semiconductor division accounted for more than half of the total operating profit. Its sales share is 32%. Samsung manufactures sets (finished products), semiconductors, and displays, but it is a company stronger in the components business. Component companies such as SK Hynix and LG Display play the role of the 'main artery' of Korean industry.

The 'components' industries such as semiconductors, displays, and packaging are in a precarious situation. Externally, due to decoupling between major markets like the United States and China, they are forced into a situation where they must choose only one customer. Internally, uncertainties are increasing due to regulations and complex transactional relationships with set manufacturers' buyers.

Fundamentally, the set industry is structured to be easily affected by 'external winds' such as decreased customer demand and changes in device trends, but the components industry is relatively stable, with customers typically lasting for 10 years. Since it is a market coveted by everyone (every country), once leadership is lost in the competition, it is difficult to regain. In the case of semiconductors, building a single factory costs 20 to 30 trillion won, and since components are closely related to security, countries that are not 'superpowers' find it difficult to recover if they are pushed out of the mainstream.

Recently, the components industry has fallen into a 'complex crisis' all at once. Given that competing countries include superpowers such as the United States, China, Japan, Germany, and Taiwan, the sense of crisis felt by companies is even greater. Looking in detail, semiconductors are struggling with customer acquisition, displays with securing materials, and packaging with portfolio diversification issues.

The semiconductor industry is shifting its focus from memory semiconductors to system semiconductors such as foundry (semiconductor contract manufacturing) and mobile application processors (AP). As of the third quarter, the market shares of the top system semiconductor companies, Taiwan's TSMC and Samsung Electronics, are 56.1% and 15.5%, respectively, showing about a fourfold difference. Meanwhile, Korea's world-leading memory semiconductor sector is gradually being pushed out from the center of the market. Samsung Electronics' memory semiconductor sales ratio compared to third-quarter sales over the past five years dropped from 32.2% → 21.4% → 21.3% → 28.2% → 19.8%.

The problem is that without securing customers, it is difficult to successfully operate businesses like foundry and mobile AP. Leading global set companies such as the United States' Apple and CPU manufacturer Intel continue to turn to TSMC rather than Samsung Electronics. TSMC recently announced mass production of 3-nanometer products and declared its intention to close the six-month gap with Samsung Electronics. Even if it continues to win in the cutting-edge competition such as 2-nanometer technology, the failure to attract customers during the six-month lead at 3-nanometer directly translates into the market share gap.

In the display sector, issues such as securing materials, competing in cutting-edge technology, and financial risks need to be resolved. The domestic material localization rate is about 60%, which is not low and seems unproblematic at first glance. However, the market-leading products are changing. The industry is transitioning from LCD (liquid crystal display) to OLED (organic light-emitting diode) and microLED, an inorganic light-emitting diode, as mainstream products. OLED is also shifting from products used in mobile devices to those used in tablets and laptops. It is necessary to secure customers who will purchase products steadily.

Similar to the foundry market in semiconductors, the display industry is in a frustrating situation where it wins in technology but fails to gain market share. Korea's global market share remained at 33% last year, losing first place to China at 42%. Although support measures such as doubling the investment tax credit rate are being implemented, critics say it is too late after the LCD market was devastated.

Rather, the private sector is more proactive. The Display Materials Subcommittee, consisting of 18 domestic material companies including Mirae Nanotech, Dongwoo Fine-Chem, and Duksan Neolux, along with the Korea Display Industry Association, has officially requested government support while promoting international research and development (R&D) on materials used in foldable phone glass. The committee plans to collaborate on R&D for inkjet (OCR) and ultra-thin encapsulation materials with organizations such as the U.S. Cativa and Germany's Fraunhofer.

In the case of substrate packaging, represented by companies like Samsung Electro-Mechanics, the situation is better than semiconductors and displays but the status as a 'follower' remains unchanged. They are lagging behind world leaders such as Japan's Ibiden and Showa Denko, and Taiwan's Unimicron. Ibiden is collaborating with TSMC, widening the gap with Korea's top company Samsung Electro-Mechanics. Major domestic companies Samsung Electro-Mechanics and LG Innotek are competitively increasing investments, identifying server-use FC-BGA (flip-chip ball grid array) substrates as future growth engines. They believe it is difficult to rely solely on existing MLCC (multilayer ceramic capacitors) and camera module businesses.

Kim Yangpaeng, a senior researcher at the Korea Institute for Industrial Economics & Trade, said, "Korea's industrial development focused more on finished products rather than basic science and basic components, so set companies were dominant and core materials, components, and equipment were mostly imported, but the importance of components has always been very high. As Korea's industrial structure shifts to a 'developed country model,' the importance of materials, components, equipment, and basic science increases, naturally expanding the role of component companies, so government support needs to be significantly expanded."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}

{kind=link}