[Asia Economy Sejong=Reporter Kim Hyewon] As the Yoon Suk-yeol administration's first budget bill fails to pass the National Assembly due to disagreements between the ruling and opposition parties over corporate tax, attention is turning to the effectiveness of corporate tax cuts. Beyond the political framing of 'tax cuts for the rich,' did investment and employment actually increase during the Lee Myung-bak administration, which previously lowered the top corporate tax rate? The answer is 'yes.'

According to the Ministry of Economy and Finance, the Korea Development Institute (KDI), and the Korea Economic Research Institute on the 16th, total investment from 2009 to 2012 increased by more than 100 trillion won compared to 2005 to 2008. This statistic shows that the effect of lowering the top corporate tax rate from 27.5% to 24.2% during the Lee Myung-bak administration positively influenced corporate investment with a lag of one to two years. At that time in 2008, the investment scale of domestic listed companies was in the low 50 trillion won range but rebounded to the mid-60 trillion won range after the corporate tax rate cut. Especially considering that 2009 was the first year when the impact of the global financial crisis fully materialized, it means that companies could deploy the investment capacity relatively secured by paying less corporate tax to cope with the crisis. The National Bureau of Economic Research (NBER) recently stated, "Corporate tax cuts lead to sustained increases in gross domestic product (GDP) and productivity," adding that "the effects peak between five and eight years."

Overseas cases where lowering corporate tax rates actually promoted economic growth are worth noting. The United States significantly cut its corporate tax rate from 35% to 21% in 2017 and showed the highest economic growth among major advanced countries until 2019, just before the COVID-19 pandemic. Ireland halved its corporate tax rate, and its national income rapidly grew from $30,000 to $50,000 within four years.

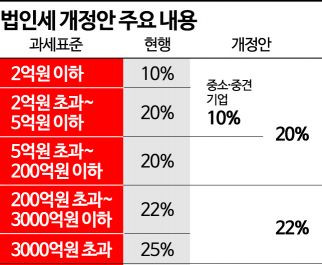

In the National Assembly, a power struggle is ongoing between the ruling and opposition parties over a mediation proposal to lower the corporate tax rate by 1 percentage point. Regarding these figures, academia has also provided evidence of the correlation between corporate tax adjustments and investment and employment. Kim Hak-soo, a senior research fellow at KDI, analyzed that a 1 percentage point reduction in the top corporate tax rate leads to short-term increases of 0.46% in investment and 0.13% in employment. In the long term, investment and employment increase by 2.56% and 0.74%, respectively. Based on GDP, short-term growth is estimated at 0.21%, and long-term growth at 1.13%. Conversely, a regression analysis commissioned by the Korea Economic Research Institute and conducted by Professor Hwang Sang-hyun of Sangmyung University found that a 1 percentage point increase in the top corporate tax rate reduces investment relative to total assets by 5.66 percentage points and decreases the number of employees by 3.53%.

While corporate tax cuts immediately reduce national tax revenue, statistics also show that from a long-term perspective, they contribute to fiscal expansion through increased tax revenue. From 2009, when the Lee Myung-bak administration implemented corporate tax cuts, until just before the Moon Jae-in administration raised the top corporate tax rate again, corporate tax revenue actually increased by 23.9 trillion won over nine years. The top corporate tax rate steadily decreased from 34% in 1993 to 22% before the Moon administration, which then raised it by 3 percentage points to 25%.

Compared to global standards, South Korea's relatively high corporate tax is pointed out as a factor that diminishes the attractiveness of domestic investment for foreign companies. The head of a domestic foreign investment attraction agency said, "If a multinational company A chooses a location for its regional headquarters or factory among Japan, China, Taiwan, Singapore, and Korea, Korea is typically avoided due to excessive taxes such as corporate and income taxes, and secondly, because of high labor costs relative to low labor productivity." In fact, since the corporate tax rate increase in 2018, foreign investment in Korea has steadily declined, halving to $5 billion.

Among 38 OECD countries, only South Korea and Costa Rica apply a progressive tax rate with four or more tiers. The Ministry of Economy and Finance stated, "The reason major countries operate a single corporate tax rate system is that multi-tiered progressive tax rates hinder corporate growth and cause inefficiencies such as artificial splitting to avoid high progressive rates."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}