[Asia Economy Reporter Changhwan Lee] # Mr. A was diagnosed with hypothyroidism three years ago and took hormone medication, but he marked 'No' to all pre-contract disclosure questions on the insurance application form and signed it by hand before the contract was finalized. Later, when the insurance company notified him of contract termination due to failure to disclose past medical history during the claim process, he claimed to have verbally informed the agent and filed a complaint with the Financial Supervisory Service.

# Mr. B recently reviewed his insurance details and found that he had duplicate coverage for injury medical expenses, resulting in double premium payments. He had recently subscribed to driver insurance, but the agent had redundantly enrolled him in injury (actual expense) medical coverage without explanation, prompting him to file a complaint with the Financial Supervisory Service.

The Financial Supervisory Service disclosed on the 26th key points that insurance consumers should be aware of when subscribing to non-life insurance products based on recent major complaint case analyses.

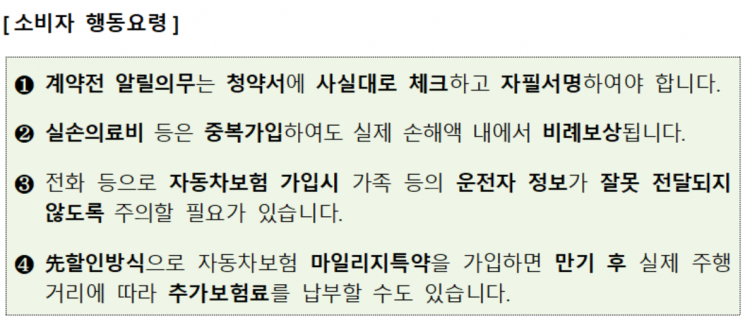

The Financial Supervisory Service emphasized that under the pre-contract disclosure obligation, insurance consumers (policyholders or insured persons) must truthfully inform the insurance company of all matters asked in the pre-contract disclosure section of the application form.

Generally, the pre-contract disclosure obligation is fulfilled by recording the information on the application form and notifying the insurance company. Even if the consumer recalls verbally informing the insurance agent, if there is no evidence to prove this and the application form contains inaccurate information, the insurance company can claim contract termination and denial of claim payment based on the application form.

It was also noted that for actual expense medical coverage, duplicate subscriptions result in proportional compensation only within the actual loss amount.

Actual expense-type coverage includes personal/group actual medical expenses, daily life liability insurance, fire insurance, and driver insurance covering fines, criminal settlement fees, and attorney fees.

The Financial Supervisory Service stressed that since these products provide proportional compensation within the actual loss amount even if subscribed to multiple times, consumers should avoid duplicate subscriptions except for purposes such as expanding coverage scope or increasing coverage amounts.

On the other hand, fixed-amount coverage such as daily hospital allowance and diagnosis fees pay the insured amount specified in each insurance contract separately when an insured event occurs.

Additionally, when subscribing to driver-specific special clauses in automobile insurance (such as single driver limitation, age limitation, spouse/family limitation), consumers must be especially careful as providing incorrect information may result in insurance being subscribed against their will and claims being denied.

The insurance company does not verify the validity of information such as the birthdates of family members or other drivers, so consumers must accurately submit driver information, check for errors, and additionally verify the application form or insurance policy issued by the insurance company.

Furthermore, regarding mileage discount clauses, the advance discount method provides a discount based on the expected mileage at the time of contract, but if the actual mileage at maturity exceeds the agreed mileage, additional premiums will be charged, so consumers should be aware of this as well.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}