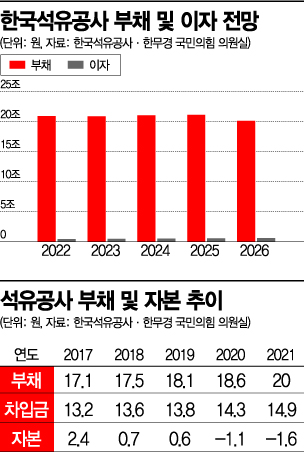

Korea National Oil Corporation's Debt Hits 20.9 Trillion Won This Year, Up 1 Trillion in One Year

Capital Deficit Expected Until 2026...Half of Operating Profit Goes to Interest Expenses

Asset Sales Have Limited Impact...Concerns Over Supply Chain Instability

Kim Dong-seop, President of Korea National Oil Corporation, presiding over the 'Oil Crisis Response Task Force (TF)' situation review meeting last March. [Photo by Korea National Oil Corporation]

Kim Dong-seop, President of Korea National Oil Corporation, presiding over the 'Oil Crisis Response Task Force (TF)' situation review meeting last March. [Photo by Korea National Oil Corporation]

[Asia Economy Sejong=Reporter Lee Jun-hyung] Korea National Oil Corporation's disposal of the Anchor oil field in the U.S. Gulf of Mexico at a bargain price was due to the urgent need for restructuring to normalize management. The financial structure of the Oil Corporation, which entered an emergency management system in 2018, had already exceeded its limits several years ago. The debt ratio, an indicator showing the company's financial soundness, soared nearly fivefold in just two years, from 719% in 2017 to 3,415% in 2019. Eventually, the Oil Corporation fell into complete capital erosion in 2020.

The problem is that even continuous sales of overseas assets make it difficult to overcome capital erosion. According to the "2022-2026 Mid-to-Long-Term Financial Management Plan" submitted by the Oil Corporation to the office of Han Mu-kyung, a member of the People Power Party, the Oil Corporation is expected to remain in a state of capital erosion until 2026. Debt is projected to increase by nearly 1 trillion KRW in one year, from 19.963 trillion KRW last year to 20.8946 trillion KRW this year. The Oil Corporation's debt is expected to remain in the 20 to 21 trillion KRW range over the next five years, from this year through 2026.

Annual Interest Costs of 500 Billion KRW

As debt increases, the cost paid as interest is also substantial. The Oil Corporation's interest expenses steadily rise, amounting to 415.4 billion KRW this year, 454.9 billion KRW next year, and 505 billion KRW in 2024. In 2026, it will spend 574.7 billion KRW on interest expenses, which is more than half of its operating profit (1.0899 trillion KRW). This explains why the debt hardly decreases even though the operating profit exceeds 1 trillion KRW annually.

Given this situation, the Oil Corporation views government financial support as inevitable. Due to astronomical debt, annual interest expenses alone reach several hundred billion KRW, and internal efforts such as asset sales have limitations in improving the financial structure. The Oil Corporation stated in the mid-to-long-term financial management plan submitted to the Ministry of Economy and Finance at the end of last month that "minimum additional government financial support is necessary to normalize management and restore resource security functions," reflecting the same context.

There are also concerns that the overseas asset restructuring aimed at improving the financial structure should be reconsidered from the beginning. The effect of asset rationalization is not as significant as expected, with debt exceeding 20 trillion KRW until 2026. Since the Oil Corporation has focused more on "sale" than "price" in selling overseas assets, its bargaining power in price negotiations has weakened, raising concerns about the possibility of bargain sales.

Korea National Oil Corporation's offshore Anchor oil field in the U.S. Gulf of Mexico, sold last July.

Korea National Oil Corporation's offshore Anchor oil field in the U.S. Gulf of Mexico, sold last July. [Photo by Korea National Oil Corporation]

Concerns Over Supply Chain Instability

From a long-term perspective, there is also a view that selling overseas assets may cause more harm than good. In a situation where major countries are weaponizing resources, the Oil Corporation's "mass sale" of overseas assets could exacerbate domestic supply chain instability. In fact, the Oil Corporation's production volume has decreased by about 41%, from 237,000 boed (barrels of oil equivalent per day) in 2015 to 136,400 boed last year due to successive asset sales. The Anchor oil field, sold for less than half of the total investment cost, had proven oil and gas reserves of 24.4 million barrels as of the end of last year and was an offshore oil field producing 3,000 barrels per day.

Concerns about hasty sales are not limited to the Oil Corporation. Public enterprises designated as "financial risk institutions" by the government, such as Korea Electric Power Corporation (KEPCO), are undertaking large-scale overseas asset restructuring. KEPCO, which posted a deficit of 14.3033 trillion KRW in the first half of this year alone, plans to sell the Cebu power plant in the Philippines and the Boulder 3 solar power plant in the U.S. within this year as part of financial structure improvement. KEPCO is also accelerating domestic asset restructuring, including considering the partial sale of the KEPCO Art Center in Seocho-gu, Seoul, which was regarded as a "prime real estate."

The Korea Mining Development Corporation (KOMIR), which was at the forefront of resource diplomacy during the Lee Myung-bak administration, is in a similar situation. KOMIR is proceeding with the sale process to dispose of 13 out of 15 overseas mines it holds. Through such overseas asset restructuring, it plans to reduce its debt from 7.2642 trillion KRW last year to 5.1902 trillion KRW in 2026, lowering it by more than 2 trillion KRW.

Professor Son Yang-hoon of Incheon National University's Department of Economics, former president of the Korea Energy Economics Institute, said, "For a country like Korea, which has a high dependence on energy imports, selling overseas assets is not a wise choice," adding, "Overseas resource development should be pursued based on economic and scientific facts, not political logic."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}