Comparison Disclosure of Loan-Deposit Interest Rate Spread, Bank-to-Bank Comparison Possible... Reporting Period Shortened to 1 Month

Improvement in Disclosure of Loan and Deposit Interest Rates

[Asia Economy Reporter Song Hwajeong] With the commencement of the disclosure comparing the interest rate spread between deposits and loans, consumers can now compare the interest rate spreads of different banks as well as check the interest rate spreads by credit score segments.

On the 22nd, the Korea Federation of Banks announced that from this day forward, it has started disclosing the interest rate spread comparison on the consumer portal of the Federation of Banks website and improved the disclosure of loan and deposit interest rates.

This improvement in the disclosure system was promoted to alleviate consumers' burdens during the period of rising interest rates by providing accurate and sufficient interest rate-related information to consumers.

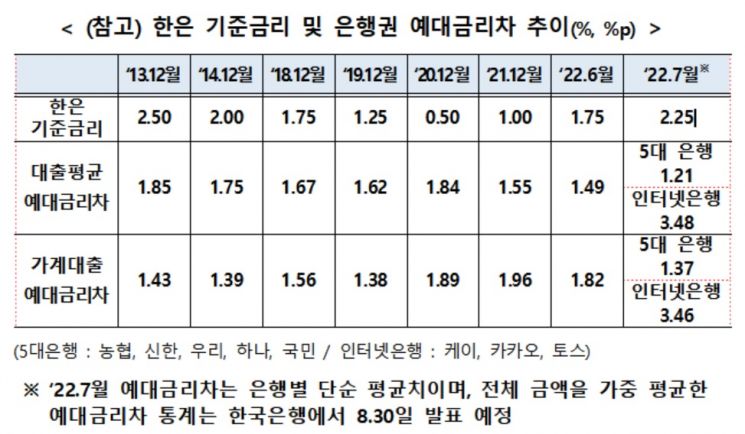

The interest rate spread comparison disclosure publicly compares the interest rate spreads of all banks and shortens the disclosure cycle from the previous three months to one month. Previously, individual banks disclosed their own interest rate spreads as one of the management disclosure items, making it difficult to compare between banks and providing information with a long delay, which hindered timely information provision. The interest rate spread is calculated by subtracting the interest rate on savings deposits from the average loan interest rate, based on the weighted average interest rate of financial institutions by the Bank of Korea. The average loan interest rate is the weighted average interest rate of newly issued household and corporate loans in the relevant month, and the interest rate on savings deposits is the weighted average interest rate of newly issued pure savings deposits (such as time deposits and installment savings) and market-type financial products (such as CDs and financial bonds) in the relevant month (excluding demand deposits and passbook savings).

The interest rate spread is calculated based on the amount of new transactions to allow monthly trend tracking and discloses both the average loan (household + corporate) based and household loan based interest rate spreads. In particular, the household loan based interest rate spread is also disclosed by credit score segments to make it easier for consumers to utilize. A representative from the Korea Federation of Banks explained, "In banks with a high proportion of loans to middle- and low-credit borrowers, the average interest rate spread may widen, but by disclosing the interest rate spread by credit score segments, we aimed to resolve misunderstandings."

The interest rate spread can expand or contract depending on the loan and deposit portfolio of each bank. For example, when the proportion of loans to middle- and low-credit borrowers is high, the interest rate spread expands. Based on new transactions in July, the average for the five major commercial banks was 14.3%, while the average for internet banks was 31.1%. The interest rate spread also expands when the proportion of mortgage loans is low and the proportion of unsecured loans is high. Toss Bank’s interest rate spread expanded as it only handles unsecured loans without collateral. The interest rate spread also expands when the proportion of policy products for low-credit borrowers is high. Jeonbuk Bank’s interest rate spread expanded due to a high proportion of loans linked to the Korea Inclusive Finance Agency’s products such as the Sunshine Loan Bank and Sunshine Loan Youth. The interest rate spread also expands when the basic interest rate on deposits and savings is low but the preferential interest rate confirmed at maturity is high. Conversely, the interest rate spread contracts when the proportion of financial bond issuance is high or when deposits are raised at high interest rates for liquidity management.

Additionally, the disclosure standard for loan interest rates has been changed from the bank’s own credit rating system (5 levels) to the credit score of credit rating agencies (CB) (9 levels, in 50-point increments) starting from new transactions in July. While consumers can always check their own credit scores based on credit rating agencies through affiliated platforms, it was difficult for consumers to check the credit ratings calculated by banks. With this change in disclosure standards, it is expected that consumers will be able to easily check and compare interest rate information that matches their own credit scores. However, since the actual loan conditions are determined based on the bank’s own credit rating at the time of the loan, consumers should inquire with the respective bank for detailed information such as interest rates and limits.

Furthermore, the interest rate information (basic interest rate, highest preferential interest rate) of major deposit products sold by banks now also includes the average interest rate of the previous month (new transactions) in the disclosure. Since the criteria for preferential interest rates vary by bank, it was previously difficult for consumers to confirm the actual applied interest rate information. With this improvement in disclosure, consumers are expected to be able to check the actual applied deposit interest rate information and use it when selecting deposit products.

A representative from the Korea Federation of Banks stated, "Through this improvement in disclosure, it is expected that the accessibility of accurate and sufficient interest rate information for financial consumers will be greatly enhanced," and added, "We will monitor the impact of this improved disclosure system on loan and deposit interest rates and consumer burdens in the banking sector during the first half of next year."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}