Profitability Deterioration Due to Interest Rate Hikes

Bridge Loans Virtually Halted

Increased Risk for Small and Medium Firms

[Asia Economy Reporter Minji Lee] As the real estate market walks on thin ice, project financing (PF) has become a 'worry' for securities firms. With profitability deteriorating due to rapid interest rate hikes and soaring raw material prices, and increasing risks of insolvency, some securities firms have started to 'tighten lending.'

According to the investment banking (IB) industry on the 12th, securities firms that had been expanding their real estate PF business scale are recently almost halting 'bridge loans.' With the combination of interest rate hikes and increases in raw materials and construction costs, Meritz Securities has virtually stopped bridge loans. Small and medium-sized securities firms such as Daol Investment & Securities, Hanwha Investment & Securities, and IBK Investment & Securities have also tightened the screening criteria for bridge loans. A representative from a small to medium-sized securities firm said, "Last year, when the real estate market was rising, about half of the 10 cases submitted for screening passed, but now it is difficult for even one to pass."

The role of securities firms in real estate PF is to gather funds from major lenders such as banks and insurance companies and provide financing to developers. Typically, developers receive interim and final payment loans from securities firms for land acquisition before starting PF, which is called a bridge loan. Recently, it also includes contract payment loans (10% of the land purchase price) made at the very early stage of the project. In terms of risk, bridge loans that start at the early stage of the project are even larger than the main PF.

The connection to PF is the most critical part of bridge loans. If financing, land acquisition, and permit risks are not resolved and the transition to PF does not occur, securities firms inevitably face losses. Recently, as borrowing costs have risen, it has become difficult for developers to refinance existing loans with new loans, increasing the burden on securities firms. When not connected to PF, funds must be re-raised through bridge loans, and while interest rates were previously around 5-6%, they have recently risen to 8-10%, increasing cost burdens.

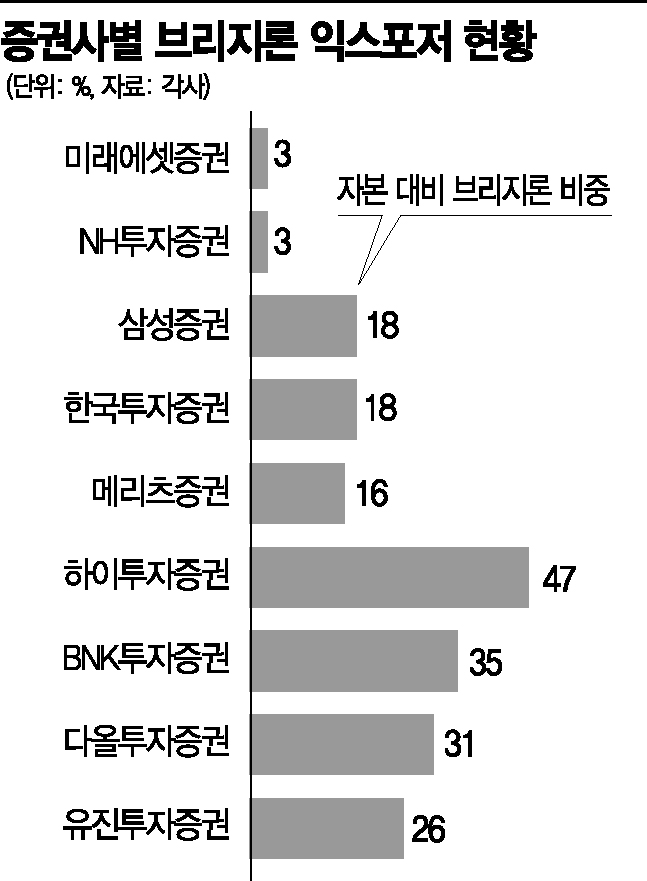

Small and medium-sized securities firms are more concerning than large securities firms. Because higher risk allows for higher interest income, small and medium-sized securities firms have been actively conducting business. Looking at the proportion of bridge loans relative to capital by securities firm, Hi Investment & Securities has the highest at 47%, followed by BNK Investment & Securities (35%), Daol Investment & Securities (31%), Hyundai Motor Securities (31%), Kyobo Securities (29%), and Eugene Investment & Securities (26%). While logistics centers and industrial complex properties are considered relatively stable, most are residential complexes with high insolvency risks. Another representative from a small to medium-sized securities firm lamented, "Given the current atmosphere, securities firms will have no choice but to downsize and reorganize their PF teams by the end of the year," adding, "The notion that working in the PF department means making a lot of money is all in the past."

Credit rating agencies have also issued unified warnings about the high possibility of future insolvency in securities firms' PF businesses. Yeri Lee, Senior Researcher at NICE Credit Rating's Financial Evaluation Division, pointed out, "In a situation where financial market uncertainty is expanding, if the real estate market deteriorates, refinancing risks could escalate rapidly," adding, "There is a high possibility that the number of projects classified as delinquent, centered on bridge loans, will increase, which could expand securities firms' losses."

Jaewoo Lee, Senior Researcher at Korea Credit Rating's Financial Structuring Evaluation Division, also analyzed, "For small and medium-sized firms with many bridge loans, if real estate collateral values fall by 30%, losses equivalent to 20-30% of capital could occur," and "It will be unavoidable to see a decline in performance due to the contraction of real estate financing, one of the main revenue sources for securities firms."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}