Combining the Advantages of Public and Private Equity Funds

Easier Capital Recovery through Listing on Korea Exchange

[Asia Economy Reporters Ji Yeon-jin and Lee Jung-yoon] A 'Growth Enterprise Investment Fund' that combines the investor protection mechanisms of public funds with the flexible management strategies of private funds is being promoted. This fund mandates listing, allowing investors to trade shares like stocks, making it easier to recover investment funds. It also offers the advantage of investing in unlisted stocks through a stable fund managed by professional asset managers.

The Financial Services Commission announced on the morning of the 26th, at the Cabinet meeting, that the amendment to the Capital Markets Act was approved. This amendment introduces a corporate growth collective investment scheme that focuses on venture and innovative companies and enables investment recovery through listing.

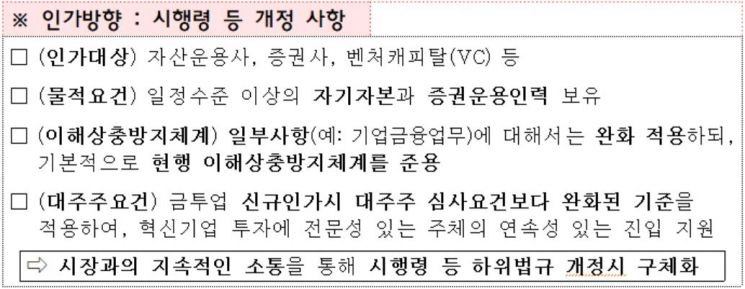

This new type of fund will be operated by competent and responsible entities such as asset management companies, securities firms, and venture capital (VC) through an approval system, and will be established as a closed-end fund (with restrictions on mid-term redemptions) lasting at least five years. There is also a plan to stipulate the minimum fundraising amount through enforcement ordinances to create funds of substantial scale.

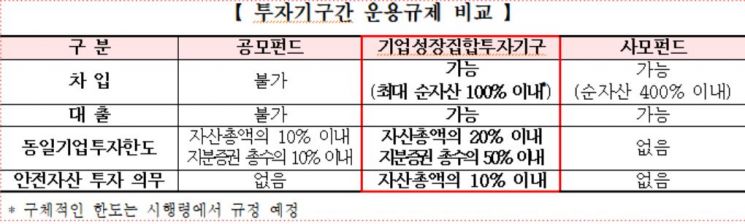

Borrowing and lending are permitted to supply funds according to investment targets, and there are safety measures such as mandatory investment of at least 10% of total assets in government bonds or monetary stabilization bonds, and regulations on investment limits in the same company to ensure asset management safety.

A certain proportion of the fund’s assets must be invested in venture and innovative companies, and it will be operated as a redemption-prohibited (closed-end) fund to enable companies to raise funds over the long term.

Additionally, to address the difficulty early investors face in recovering funds due to long-term redemption restrictions, listing on the exchange is mandatory within 90 days. Although it is a redemption-prohibited fund, investors wishing to recover funds during the fund’s duration can do so by trading securities on the Korea Exchange.

Furthermore, while applying investor protection measures of public funds such as regular and ad hoc disclosures, the fund manager is required to make a seeding investment by holding a certain proportion of the fund, and the disclosure scope of major management matters of investee companies will also be expanded.

Until now, investments in venture or innovative companies have been handled by policy finance or venture capital (VC), often supported by the Korea Fund of Funds or providing relatively small-scale funds mainly to early-stage or startup companies. Public funds have been reluctant to invest in unlisted companies with low liquidity due to the premise of frequent redemptions, and institutional private equity funds (formerly PEFs), which have a strong venture capital nature including management participation, have prohibited general public participation.

As a result, small individual investors have invested in growth companies in the unlisted stock market. However, there have been many criticisms that investment in these growth companies tends to be 'blind investment' due to difficulties in accessing information and limitations in analyzing companies. A Financial Services Commission official said, "With professional operators entering and being regulated, it will shift to professional indirect investment," adding, "This new type of growth enterprise fund can reduce blind investments."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}