Domestic Market Share LCC No.1

High Passenger Focus Leads to Growing Losses

Rosy Outlook for Profit Turnaround Next Year

Concerns Over Capital Erosion Before Passenger Recovery

[Asia Economy Reporter Park Jihwan] Jeju Air is considered the undisputed number one among domestic low-cost carriers (LCCs). The easing of government regulations on domestic arrivals and the relaxation of travel restrictions worldwide due to the COVID-19 pandemic are common favorable factors for the LCC industry. Among them, Jeju Air holds a comparative advantage with the largest fleet of about 40 aircraft. It is expected to show the fastest recovery once travel fully resumes.

Jeju Air was established in 2005 as a joint venture between Jeju Special Self-Governing Province and the Aekyung Group. The largest shareholder is AK Holdings, the holding company of Aekyung Group, holding 53.39% of shares. Other major shareholders include the National Pension Service (8.04%) and Jeju Province (6.10%). Through continuous route development and preemption in domestic routes, China, Japan, Taiwan, and Oceania, Jeju Air maintains its position as the number one domestic LCC.

Most of the revenue is generated from passenger transportation. As of the third quarter of last year, 95.22% of total revenue came from passenger transportation income. Cargo transportation accounted for only 2.20%. Particularly in domestic routes, Jeju Air holds nearly a 20% market share, surpassing Korean Air (14.1%) and Asiana Airlines (13.4%) to become the top operator. Its international route market share is about 1.9%, which is not comparable to foreign airlines (40.6%), Korean Air (31.6%), and Asiana Airlines (20.8%), but it is the highest among LCCs. The revenue distribution by country is Southeast Asia (40.5%), Japan (24.3%), and China (19.2%) in that order.

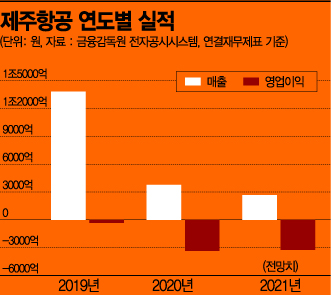

Jeju Air’s performance began to falter starting in 2019, before the outbreak of COVID-19. Amid fierce price competition among LCCs, the Japanese boycott movement triggered by the economic provocations of the Abe Shinzo administration in 2019 dealt a direct blow. Operating profit, which had reached about 101 billion KRW in 2018, plunged to an operating loss of 32.9 billion KRW in 2019.

The boycott was just the beginning. One year later, the COVID-19 pandemic shut down air routes, causing losses to snowball. Following an operating loss of 335.8 billion KRW in 2020, a large-scale operating deficit exceeding 320 billion KRW is expected again last year. Jeju Air survived for two years through financial support and borrowings, and as borrowings increased, its debt ratio is estimated to have soared from 170% in 2018 to over 530% last year.

The general consensus in the securities industry is that if Jeju Air can endure the worst management situation this year, it will be "the end of hardship and the beginning of happiness." Although operating losses are inevitable this year, travel demand is expected to recover gradually from the second half, reflecting incremental revenue. According to FnGuide, Jeju Air is forecasted to reduce its operating loss significantly to 9.3 billion KRW this year compared to the previous year.

Next year, a turnaround to a profit of 123.7 billion KRW is anticipated for the first time in four years. Park Sooyoung, a researcher at Hanwha Investment & Securities, said, "If travel restrictions to Guam, Saipan, Bangkok, Singapore, and other destinations ease during the lull in the currently circulating variant virus, Jeju Air, which has the most aircraft among domestic LCCs, will be the biggest beneficiary."

However, the outlook is not entirely rosy. The continued operating losses of Jeju Air pose a burden due to potential capital erosion issues. If the deficit trend continues, there are concerns that Jeju Air could fall into capital erosion again before fully enjoying the passenger recovery expected in the second half of next year.

In fact, as of the third quarter of last year, Jeju Air was in a state of complete capital erosion with a negative equity of 2.45 billion KRW due to accumulated losses. Currently, it has temporarily escaped capital erosion by successfully raising capital worth 236.6 billion KRW through a free capital reduction that reduced the par value of shares to one-fifth, issuance of perpetual bonds, and a paid-in capital increase.

Jung Yeonseung, a researcher at NH Investment & Securities, said, "Jeju Air’s liquidity continues to be depleted as the recovery of air passenger demand is delayed due to the spread of the COVID-19 Omicron variant. Although passenger demand is expected to gradually recover from the end of this year and profitability is expected to improve with rising passenger fares, there is a possibility that Jeju Air will seek additional capital expansion within this year to endure the liquidity depletion period until demand recovers."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}