All Five Major Banks Reflect Interest Rate Hikes on Deposits on the 20th

Loan Rates May Rise Further with a Time Lag

[Asia Economy Reporter Park Sun-mi] Although the five major commercial banks have applied the full increase in deposit interest rates, it is expected to be difficult to narrow the loan-deposit interest rate spread (loan interest rate - deposit interest rate) due to the rapid rise in loan interest rates. While putting money into bank time deposits still yields a meager interest rate in the 1% range, credit loan interest rates are on the verge of surpassing 5% per annum, raising concerns that banks will continue to profit excessively.

According to the banking sector on the 20th, all five major banks?KB Kookmin, Shinhan, Hana, Woori, and NH Nonghyup?have reflected the Bank of Korea’s 0.25 percentage point base rate hike by raising the interest rates on deposit products by up to 0.4 percentage points. Some banks started applying the increase as early as the 17th, and even the slowest have implemented it by today. This is a deposit interest rate increase larger than the base rate hike.

However, banks have applied the 0.4 percentage point increase only to a few products, and the rate hikes vary by product, so most remain close to the base rate increase level. Except for some high-interest special promotional products, regular time deposits generally offer interest rates in the 1% range, and installment savings accounts are around 2%.

When the base rate rises, deposit interest rates usually increase first, followed by loan interest rates after a time lag to reflect higher funding costs, so loan interest rates are likely to rise further soon. Currently, mortgage loan rates at commercial banks have exceeded the mid-5% range as the COFIX (Cost of Funds Index), which influences variable mortgage loan rates, has risen rapidly. Credit loan interest rates are also on the verge of breaking through 5% per annum. Since the COFIX rate reflects the cost banks incur to raise funds through deposits and bank bonds, it rises alongside deposit interest rates.

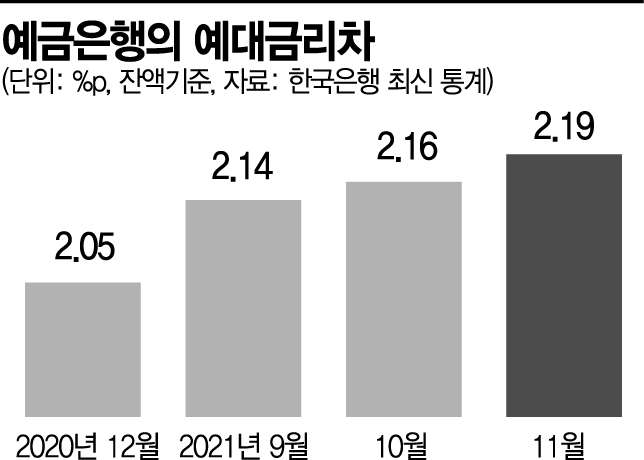

The loan-deposit interest rate spread has already been widening during this rate hike period. According to the latest data from the Bank of Korea, as of November last year, the balance-based loan-deposit interest rate spread in the banking sector was 2.19 percentage points, expanding by 3 basis points from the previous month. The spread, which was 2.05% at the end of 2020, increased to 2.14% in September 2021, 2.16% in October, and 2.19% in November.

A representative from a commercial bank explained, "With loan interest rates already rising rapidly, loan rates inevitably have to increase as deposit rates rise, so it is structurally difficult to narrow the loan-deposit interest rate spread gap for the time being." Since banks consider maintaining a certain level of net interest margin when setting deposit and loan interest rates, a partial increase in deposit rates alone does not lead to a noticeable easing of the loan-deposit interest rate spread for consumers.

The problem is that there is no clear breakthrough to resolve this, so the burden on consumers due to the widening loan-deposit interest rate spread and the additional profits for financial companies may continue for some time. Although financial authorities are closely monitoring the trend of the loan-deposit interest rate spread, it is difficult to intervene in banks’ interest rate decisions, which are effectively left to their discretion.

On the same day, Financial Supervisory Service Governor Jeong Eun-bo responded to reporters’ questions regarding the loan-deposit interest rate spread, stating that they are currently reviewing the situation. Governor Jeong said, "The Financial Supervisory Service is at the stage of inspecting loan interest rates following the review of deposit interest rates in the banking sector," and added, "Based on individual bank inspections, we understand that the recent trend shows a narrowing of the loan-deposit interest rate spread."

In the political arena, there have even been pledges to address the expanded loan-deposit interest rate spread. Yoon Seok-yeol, the presidential candidate of the People Power Party, announced in his “Heart-throbbing Pledge” yesterday that "commercial banks will be required to periodically disclose the gap between deposit and loan interest rates," and "if the loan-deposit interest rate spread rises sharply following changes in the base rate, we will closely examine whether there are elements of collusion to protect financial consumers."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}