Financial Services Commission to Push Deregulation Next Year

Shift in Mood Amid 'Loan Cliff' Criticism as Even Secondary Financial Sector Faces Restrictions

Experts Say "Positive... Must Avoid Token Measures"

High Credit Borrowers Face Loan Shortage Next Year... Criticism of 'Half-Measure Deregulation'

[Asia Economy Reporters Jin-ho Kim and Seung-seop Song] Financial authorities are considering excluding middle- and low-credit borrowers and policy finance from next year's household loan volume regulations, which is expected to somewhat ease the financial burden on ordinary citizens. This move is interpreted as a response to criticism that real borrowers are being pushed to a 'loan cliff' due to unprecedented loan regulations this year. However, high-credit borrowers are still expected to face difficulties obtaining loans next year, leading to criticism that this is a 'half-hearted regulatory relaxation.'

◆ Partial easing of loan regulations amid cries from middle- and low-credit borrowers = According to financial authorities on the 6th, the Financial Services Commission plans to soon discuss excluding middle- and low-credit borrowers and policy finance products from the total volume regulation. On the 3rd, Financial Services Commission Chairman Seung-beom Ko said at a press briefing, "We are considering practically excluding them from total volume management," adding, "Specific incentive measures will be finalized this month after consultation with the financial sector."

The financial authorities' announcement of a flexible and adaptive operation plan for household debt volume regulation, including this proposal, is analyzed as an intention to relieve the financial pressure on ordinary real borrowers. Although some banks have briefly resumed lending, even secondary financial institutions have been comprehensively blocked, rapidly pushing ordinary real borrowers toward a loan cliff.

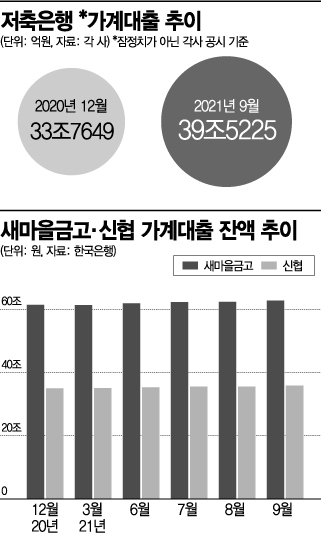

In fact, credit unions and Saemaeul Geumgo, which are mainly used by ordinary citizens, have recently completely stopped handling household loans. Other mutual finance institutions such as Nonghyup and Suhyup are also not handling new housing-related loans.

Especially, the household loan volume of savings banks, the last bastion of secondary financial institutions, is approaching this year's total volume limit (21.1%). According to the industry, as of September, the household loan volume of savings banks was 39.5225 trillion KRW, leaving only 1.3688 trillion KRW before reaching the total volume limit. Considering the increases in October and November, industry insiders explain that the remaining loan capacity is practically very limited.

Primary financial institutions also find it difficult to actively provide loans since next year's total volume regulation level will be determined based on compliance. As of the end of last month, the average household loan growth rate of the five major banks was 4.61%, leaving less than 0.4 percentage points from the 5% limit set by financial authorities. Although some banks have recently resumed lending, consumers' actual perception seems minimal.

It is also analyzed that criticism from real borrowers and political circles toward financial authorities has had an impact. As household loans were tightened simultaneously this year, real borrowers who could not obtain loans are directing their anger at the Financial Services Commission. On the Blue House's public petition board, it is easy to find posts stating that many damages have occurred due to the financial authorities' one-sided regulation.

Moreover, the strong criticism from presidential candidates of both ruling and opposition parties regarding the damage to real borrowers caused by sudden loan regulations likely added pressure on financial authorities. A financial sector official said, "The increased pressure from political circles ahead of the presidential and local elections has been a significant burden."

◆ Good intention but criticized as ‘half-hearted’ = Experts say the financial authorities' intention to prevent the contraction of loans used by ordinary citizens during total volume management is desirable but caution that it should not be merely a 'show.' There are concerns that if the financial authorities only review the system without implementing it or implement it minimally, it will become 'false hope' for ordinary citizens.

Professor Dae-jong Kim of the Department of Business Administration at Sejong University said, "Considering that middle- and low-credit borrowers have suffered the most from total volume regulations, increasing consideration for financially vulnerable groups is positive," but emphasized, "Rather than a slight exception from total volume regulation, full support is necessary."

Meanwhile, unlike middle- and low-credit borrowers, high-credit borrowers are expected to find it difficult to borrow money next year as well. Major banks have proposed a household loan growth target of 4.5-5% to financial authorities for next year. This is up to 1 percentage point lower than this year, raising the loan threshold further.

The individual Debt Service Ratio (DSR) will also be fully implemented six months earlier, starting next month. From January next year, for all loans exceeding 200 million KRW in total loan amount, the annual principal and interest repayment cannot exceed 40% of annual income. For real borrowers needing urgent funds at the beginning of the year, borrowing money will become significantly more difficult.

A financial sector official criticized, "Telling lenders not to lend to those who are fully capable but only to those in difficulty contradicts the basic logic of finance," adding, "From the financial companies' perspective, there is a risk that the ratio of non-performing loans could significantly increase."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}