Shinhyup to Stop New Mortgage and Credit Loans from the 30th

Saemaeul Geumgo Also Halts All Mortgage Loans from the 29th

Second-Tier Financial Institutions, the Last Bastion of Microfinance, Suspend Loans One After Another, Risking Vulnerable Groups Being Driven to Illegal Private Loans

[Asia Economy Reporters Jin-ho Kim and Seung-seop Song] Low-income and vulnerable groups who need urgent funds at the end of the year are at risk of being driven to illegal private loans. Unable to cross the high threshold of banks, they are forced to borrow money from the second-tier financial institutions where interest rates are relatively high. However, with Saemaeul Geumgo and ShinHyup announcing the suspension of loans one after another, the situation is worsening. Although there were recent reports of loan resumption centered on some banks, the loan market has fallen into complete ‘chaos’ due to the balloon effect caused by the government’s excessive total volume regulation, as loans from the second-tier financial sector have been blocked.

According to the financial sector on the 29th, Saemaeul Geumgo has suspended the sale of four types of household loan products, including housing purchase loans and balance payment loans for pre-sale houses, at 1,300 branches nationwide starting from that day. In addition, loans through loan recruitment corporations have also been restricted. They have also decided not to pay fees for all household loans secured by housing, including living stabilization funds. The date for loan resumption is undecided. (Refer to our exclusive report on the 26th: [Exclusive] Saemaeul Geumgo to fully suspend household loans from the 29th... Regulation ‘Balloon Effect’)

ShinHyup, which has 873 branches in each region, also decided not to accept applications for housing mortgage loans for home purchase purposes, including balance payment loans, from the 30th, and will also suspend personal credit loans. ShinHyup’s resumption date is also undecided.

The full suspension of housing mortgage loans by Saemaeul Geumgo and ShinHyup is largely due to the demand overflow caused by the total volume regulation, which prevented borrowers from crossing the bank threshold. Earlier in August, starting with NH Nonghyup Bank, major city and regional banks raised their loan thresholds one after another.

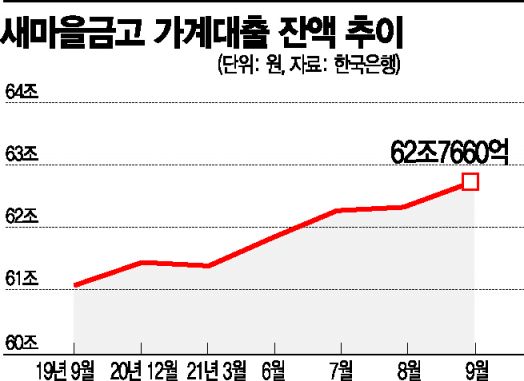

According to the Bank of Korea, the balance of household loans at Saemaeul Geumgo showed little change in the first half of this year. It increased by only 473 billion KRW over six months, from 61.394 trillion KRW at the end of last year to 61.868 trillion KRW at the end of June. However, the increase accelerated in the second half of the year. From the end of June to the end of September, it rose by 898 billion KRW in just three months.

In particular, the increase in October and November was reportedly unusually large. Although financial authorities tried to prevent the balloon effect toward second-tier financial institutions such as Saemaeul Geumgo by reducing the proportion of secured loans and requiring weekly submission of household loan increase amounts, the effect was minimal. An insider familiar with internal affairs hinted, "Due to the balloon effect caused by loan restrictions at other financial institutions, household loans at Saemaeul Geumgo surged sharply in November," adding, "It is understood that the increase exceeded the targets set by the financial authorities."

The situation is similar for ShinHyup. As of this month, it appears to have exceeded the household loan growth rate limit (4.1%) set by the financial authorities. According to the Bank of Korea, ShinHyup’s household loan balance was 35.865 trillion KRW as of September, a 2.47% (865 billion KRW) increase compared to the end of last year. Considering that the increase in September alone was about 300 billion KRW, it is estimated that the remaining limit (570 billion KRW) was greatly exceeded over the past two months.

Loan Suspensions Spread in Second-Tier Financial Sector... Double Hardship with No Place to Borrow Due to High Interest Rates

Other financial companies in the second-tier financial sector besides Saemaeul Geumgo and ShinHyup are also expected to continue tightening loans. The Financial Supervisory Service is reportedly guiding savings banks, Saemaeul Geumgo, and local Nonghyup units to lower their household loan growth targets for next year even further than this year. Considering that low-income and low-credit citizens are the main customers, it is analyzed that they will face an even more severe ‘loan famine’ than this year.

Loan regulations to be applied from next year will also raise the threshold. The Debt Service Ratio (DSR) standard for the second-tier financial sector will be lowered from 60% to 50% starting January next year. In addition, card loans, which were considered a quick source of funds, will also be included in the DSR regulation, leading to expectations of further interest rate increases.

Soaring interest rates are also increasing the burden on low-income people. In fact, mortgage loan interest rates from insurance companies have also surged. Within a month, all products with the lowest interest rates in the 2% annual range have disappeared, and products with rates exceeding 5% annually are increasing. Insurance companies are also facing significant demand that has flocked to avoid total volume regulations, but the interest rate hikes have further increased borrowers’ burdens.

The problem is that as low-income financial institutions suspend loans one after another, vulnerable groups such as borrowers who borrowed from high-interest financial companies or multiple debtors have no choice but to turn to financial companies with even higher interest rates or illegal private loans. With the base interest rate hike expected next year, loan interest rates will inevitably rise further, potentially pushing these individuals into credit delinquency.

A financial sector official said, "The second-tier financial sector is mainly used by low-income citizens, so the sudden suspension of loan handling can cause great difficulties," adding, "The impact of the total volume regulation that started in the second half of the year seems to be intensifying as the year-end approaches."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![From Bar Hostess to Organ Seller to High Society... The Grotesque Con of a "Human Counterfeit" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}