Conflict Between Financial Sector and Big Tech·Fintech Over Disclosure of Summary Information

Experts "Understand Financial Sector Concerns... Financial Authorities Must Act"

[Asia Economy Reporters Jin-ho Kim, Ki-ho Sung] Fierce competition is underway between traditional financial companies and big tech (large information and communication companies) and fintech (finance + technology) firms over the “Personal Credit Information Management Business (MyData),” which is hailed as the future growth engine of the financial sector. The two sides are clashing over issues such as the launch schedule and the scope and content of information provision, each citing “fairness controversies and competitiveness decline.” With the sudden implementation scheduled for January next year, conflicts are expected to intensify, raising concerns that it may end up as a “half-baked innovation.”

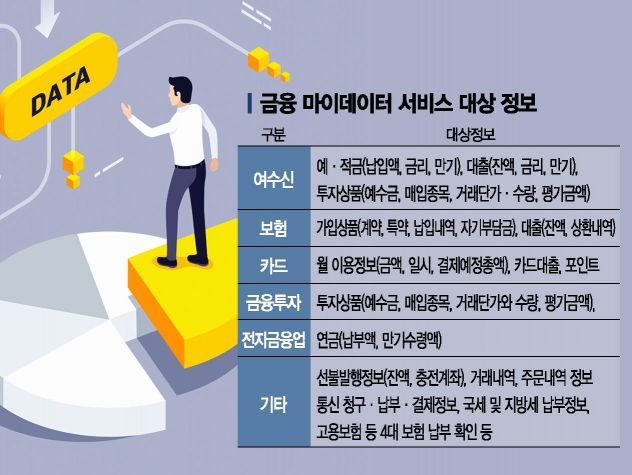

◆ Conflict Started Over Transaction Details = The conflict between traditional financial companies and big tech/fintech firms began over whether to disclose transaction details (information recording the names and memos of the sender and receiver in financial transactions), and it remains a core issue. Regarding the MyData business, banks have opposed disclosing transaction details, citing concerns over misuse and abuse of personal information. On the other hand, the big tech and fintech industries argue that for proper MyData services, users must clearly know what, how, and how much they have spent from their bank accounts.

In response, the financial authorities held a related meeting in July and ultimately decided to provide transaction details. The reason was to alleviate consumer inconvenience and enhance business effectiveness. The authorities stipulated in the guidelines that transaction details should be provided only for the purpose of consumer self-inquiry and providing analysis services about the consumer, and prohibited external provision.

However, the controversy remains heated. Voices of dissatisfaction about the so-called “tilted playing field (unfair competition)” are emerging from traditional financial companies and others. Financial firms argue that while they must disclose all customer data accumulated over decades, non-financial information held by big tech and fintech companies is not easily accessible, raising issues of “reverse discrimination.”

For example, Naver operates the MyData business through its subsidiary Naver Financial, so it does not have to disclose all information. The information provided through Naver Financial is limited to categories such as “clothing” or “food” rather than specific consumer purchase items. In contrast, banks are in a position to provide all information about customers. Due to the current data management system, it is difficult to separate sensitive information such as political party affiliation, religion, and medical-related memos from simple information like sender and receiver names, so big tech and fintech companies inevitably have to provide sensitive information.

A banking industry official pointed out, “From the bank’s perspective, the information given is core and vast, whereas the information received is limited, so there is inevitably an issue of fairness among (MyData) operators.”

Therefore, after the guideline announcement, it is reported that the banking sector recently submitted a petition to the financial authorities requesting “to ensure fairness.” They want this reflected in the final guidelines announced ahead of the full-scale implementation next year.

◆ Ongoing Fairness Controversy, Experts Say “Tilted Playing Field Must Be Resolved” = The fairness controversy can also be found in other issues. The MyData business was originally scheduled to be fully implemented from last month. However, it was postponed until the end of the year due to fintech companies’ insufficient preparation. The fintech industry requested a postponement of the mandatory API (Application Programming Interface) system for MyData, and the financial authorities accepted this.

However, from the perspective of traditional financial companies, which have devoted considerable time and money to prepare for the launch, this decision is naturally unsatisfactory. It is as if their efforts were in vain.

Also, the fact that MyData services are not available at offline bank counters is a major complaint from banks. The banking sector insists that face-to-face services are necessary to prevent the “exclusion phenomenon” of the elderly who are not familiar with digital finance, but big tech and fintech companies oppose this, citing risks such as “incomplete sales.”

Experts say the traditional financial companies’ claim of a tilted playing field is a valid point. They argue that it is unreasonable to force one side to unilaterally provide information to competitors. Professor Ji-yong Seo of Sangmyung University’s Department of Business Administration said, “For MyData to succeed, both the financial sector and big tech must open their information to each other,” adding, “It is natural for the financial sector to be dissatisfied with big tech companies demanding information while not disclosing their own sensitive data.”

He continued, “The financial authorities need to find a compromise that resolves conflicts and meets the needs of both sides,” and criticized, “Because they have not taken a more proactive approach to problem-solving, fairness controversies keep arising.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}