8 Banks Decide to Suspend Sales of 172 Complex Products

Financial Authorities Face Criticism for Delayed Administrative Rule Notification Leading to Complex Product Handling Suspension

Voices Criticize Haphazard Management... "Complacent Response and Situation Awareness"

[Asia Economy Reporter Jin-ho Kim] "It is difficult to estimate when the suspended funds can be sold again. Not only do we need board approval, but the IT systems also need to be updated, and the time is too tight. It looks like the suspension will continue for at least one to two months." (A Bank official)

The confusion in the banking sector remains even a week after the implementation of the ‘High-Risk Financial Products Recording and Cooling-Off System.’ To resume handling the approximately 170 suspended products, banks must overcome many hurdles such as board approval, revising product prospectuses, and updating IT systems. Critics point out that this situation is the result of the financial authorities’ laxity in issuing administrative rules just one week before the system’s implementation.

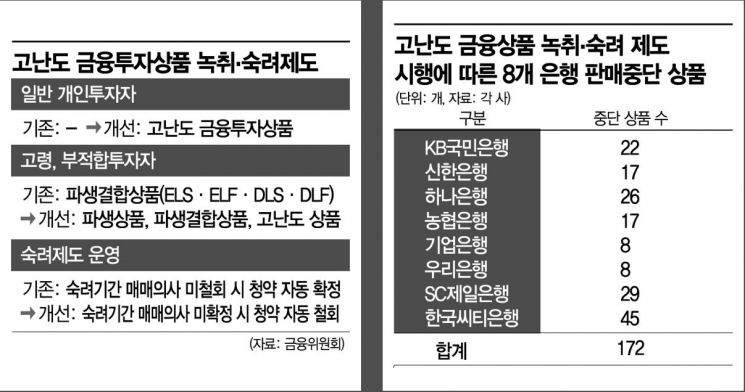

According to the financial sector on the 17th, eight major commercial banks including KB Kookmin, Shinhan, Hana, Woori, NH Nonghyup, IBK Industrial, Korea Citi, and SC First Bank have suspended sales of 172 funds (including duplicates across banks) as of that date.

KB Kookmin, Shinhan, Hana, Woori, NH Nonghyup, and IBK Industrial Bank have suspended sales of 98 funds, which is four more than the 94 funds suspended on the first day of the system’s implementation on the 10th. The two foreign-affiliated commercial banks, Korea Citi and SC First Bank, have decided to suspend sales of 74 funds. Market evaluations suggest that the number of suspended funds is likely to increase depending on decisions by asset management companies and banks.

The funds currently suspended mostly include domestic equity derivative products that incorporate Exchange-Traded Funds (ETFs) such as Samsung KOSDAQ 150, NH Amundi 1.5x Leverage Index, and Korea Investment KOSDAQ Double, as well as offshore funds investing in overseas bonds.

The suspension crisis is largely due to the ‘Partial Amendment to the Financial Investment Business Regulations,’ which defines high-risk financial products, the necessary procedures for sales, and the content required in investment briefings, being announced only on the 3rd, one week before the system’s implementation. Asset management companies that create the funds had insufficient time to classify high-risk products and revise product prospectuses, which naturally led to suspension of handling at banks.

It will likely take at least one to two months to resume sales

The suspension is expected to continue for at least one to two months. Asset management companies must first revise product prospectuses before banks can submit the matter of resuming sales as an agenda item to their boards. Holding a board meeting solely to handle this agenda is also a burden for banks, which may further delay the process.

Updating IT systems due to the system implementation is also problematic. When selling high-risk financial products, banks must record customer consultations and notify customers of investment risks and the possibility of principal loss during a two-business-day cooling-off period, all of which must be recorded in the IT system. This makes it difficult for banks to make rapid IT changes.

A B Bank official said, "Changing IT operations is not something that can be done in a short period," adding, "Under the new system, every process including staff product recommendations and customer application dates must be recorded electronically, which will take considerable time."

While the banking sector agrees with the authorities’ consumer protection intent, there is strong dissatisfaction with the haphazard handling. The crisis was already predictable when the administrative rules were announced just one week before implementation. A financial sector official said, "The financial authorities gave very little preparation time while demanding thorough work on IT system and internal regulation updates and employee training, so it was inevitable that banks would struggle to cope," criticizing, "The authorities seem too complacent about the recurring confusion whenever new systems are implemented."

In fact, this is not the first time banks have suspended product sales. When the Financial Consumer Protection Act (FCPA) was implemented in March, confusion also arose due to the failure to prepare enforcement decrees and supervisory regulations on time. The enforcement decree was finalized only a week before the law’s implementation, forcing banks to suspend sales of some loans, deposits, funds, and insurance products.

Meanwhile, the Financial Services Commission has been enforcing since the 10th the revised Capital Markets Act enforcement decree and Financial Investment Business Regulations, which require recording the sales process of complex and high-risk financial investment products and guaranteeing a cooling-off period of at least two business days. This is a follow-up measure to the 2019 overseas interest rate-linked derivative-linked fund (DLF) incident that shook the financial sector.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}