Shinhyeop TF Puts All Newly Proposed Win-Win Plans on Hold

Official: "Strong Enforcement Like Limiting Total Offices Per Union"

Large Unions Grow While Small and Medium Enterprises Sometimes Shrink

[Asia Economy Reporter Song Seung-seop] The National Credit Union Federation of Korea (NACUFOK) formed a task force (TF) to review coexistence plans among large, medium, and small cooperatives to prevent side effects from the expansion of loan service areas, but it has been confirmed that the plans were put on hold due to concerns over their coercive nature.

According to the financial sector on the 22nd, the Joint Regionalization TF under NACUFOK excluded three coexistence plans from discussion: limiting the total number of offices per cooperative, supporting priority entry for small cooperatives, and strengthening requirements for establishing branch offices.

Since May last year, NACUFOK has organized a TF involving about 100 cooperatives to review measures such as limiting the total number of offices per cooperative, tightening branch office establishment requirements, and supporting priority market entry for small cooperatives.

This was a measure to prevent widening gaps among cooperatives following regulatory easing by the Financial Services Commission (FSC). Originally, credit unions had to execute more than two-thirds of total loans to members within city, county, or district areas. The FSC expanded this to 10 nationwide zones, similar to the Saemaeul Geumgo system, allowing loans to non-members freely within these zones starting this year. The industry expressed concerns that with the expanded loan service areas, capital would concentrate in large cooperatives with strong financial power.

An NACUFOK official said, "Because it involves coercive elements, it was excluded," adding, "The contents will not come from the TF but are being discussed by the federation’s internal supervisory department." Regarding the specific announcement timing, the official said, "If a good plan comes out, we can implement it immediately," but also noted, "It is difficult to say when a decision or conclusion will be reached."

Coexistence Plans Lacking Substance: Will the Gap Among Cooperatives Narrow?

The TF plans to expand and activate currently implemented systems instead of introducing new coexistence plans. NACUFOK intends to increase linked loan programs that discover loan demanders and mediate them to small and medium-sized cooperatives, as well as performance products that entrust funds from small cooperatives for operation and profit distribution. They also mentioned the leading cooperative system, which connects large cooperatives with medium and small cooperatives in a mentor-mentee style.

However, the linked loan program and performance products have been in place since November last year, and the leading cooperative system has been implemented since 2014. This means the approach does not significantly deviate from existing alternatives. Since the specific implementation dates are undecided, there is skepticism about whether these measures can resolve the gap issue among cooperatives.

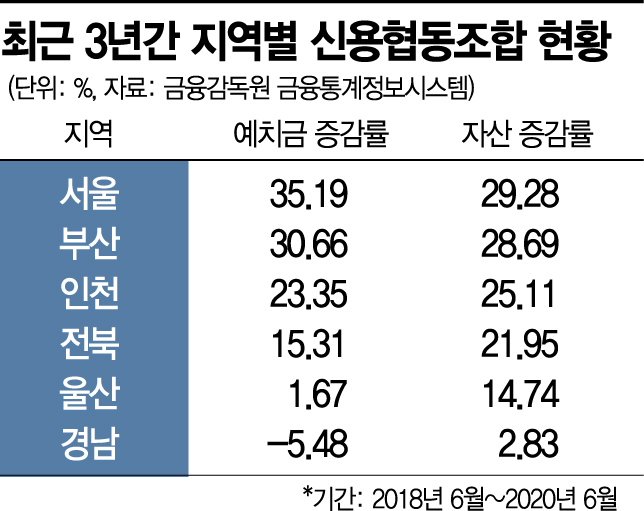

According to the semi-annual financial statements of credit unions disclosed on the Financial Supervisory Service’s Financial Statistics Information System, the gap among large, medium, and small cooperatives has been widening from June 2018 to June last year.

Larger cooperatives have seen asset growth, while smaller cooperatives have stagnated or shrunk. For example, the largest cooperative in Seoul, Eunpyeong Cooperative (assets of 460 billion KRW), increased its assets by more than 25% during this period. The second largest, Dunsol Cooperative (432.4 billion KRW), grew by 17%. In contrast, smaller cooperatives with less capital, such as Gyeongnam Samsung Gongjo Cooperative (944 million KRW) and Jeonnam Joseong Cooperative (18.2 billion KRW), experienced negative growth of 9.95% and 1.12%, respectively.

Deposits have also concentrated in relatively large cooperatives in Seoul, increasing by an average of 8.22% each half-year. During this period, deposits in Seoul expanded by a total of 35.19%. Regions with many medium and small cooperatives, such as Ulsan (0.57%) and Jeonbuk (3.66%), saw only slight increases in deposits, contrasting with Seoul. Gyeongnam, which had the lowest average growth rate (-1.27%), saw total deposits decrease by 5.48%, widening the deposit gap with Seoul from 1.6572 trillion KRW to 2.2731 trillion KRW.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}