Expected inflation already high... 1.5% is within the acceptable range of the US Federal Reserve

[Asia Economy Reporter Minwoo Lee] There is a forecast that the yield on the U.S. 10-year Treasury note could rise to 1.50%. In this case, it is analyzed that one should take a wait-and-see approach due to concerns about further increases.

On the 21st, KTB Investment & Securities analyzed the recent rise in interest rates in this way. On the 19th (local time), the yield on the U.S. 10-year Treasury note reached 1.363% intraday, the highest level in the past year. During last week (15th-19th), the yields on the 10-year and 30-year notes rose by nearly 14 basis points (1bp = 0.01 percentage points) each.

Government Stimulus, COVID-19 Vaccine Spread... Rising Oil Prices Also Expected, Leading to Inflation Expectations

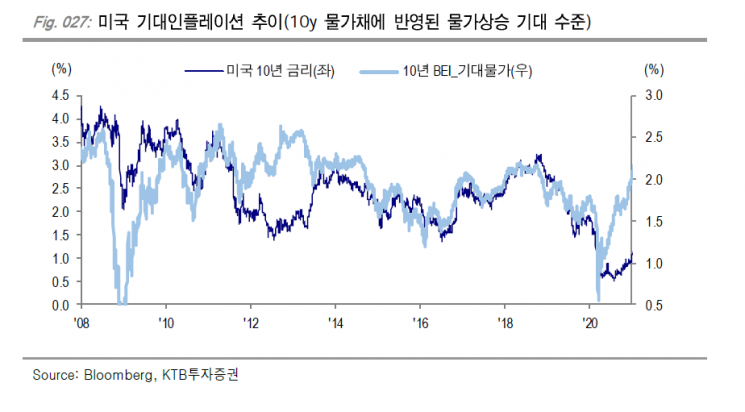

The background for this upward trend is attributed to rising inflation expectations. With support from the U.S. Federal Reserve and Treasury Department, the spread of COVID-19 vaccines, and oil production cuts leading to rising oil prices, inflation expectations have sharply increased. As of the 18th, the market's inflation expectation reflected in asset prices, separate from actual inflation, stood at 2.22%.

Researcher Jungin Heo of KTB Investment & Securities stated, "The Federal Reserve's (FED) successful high-pressure economic policy confirmed a baseline inflation increase, and aggressive fiscal policies caused inflation to rise faster than expected, increasing the possibility of the Fed's early tapering (reduction of asset purchases). This has exposed nominal interest rates to upward pressure."

It is expected to take some time for inflation expectations to translate into actual inflation increases. Although consumer sentiment is improving, the absolute number of unemployed people, especially in service sectors where work is difficult, remains high, and there is significant uncertainty about the COVID-19 situation. Nevertheless, inflation expectations are expected to continue rising.

Researcher Heo explained, "Since the Fed's current policy focuses on employment recovery, the priority is to bring back those who lost jobs due to COVID-19, tolerating side effects such as rapid inflation increases. Therefore, the Fed continues its historically large-scale asset purchases while supporting the Treasury's income preservation policies, which in itself raises inflation expectations, so we need to consider inflation expectations in the 2.50% range."

Possibility of Treasury Yield 'Overshooting' Due to Rising Inflation Expectations

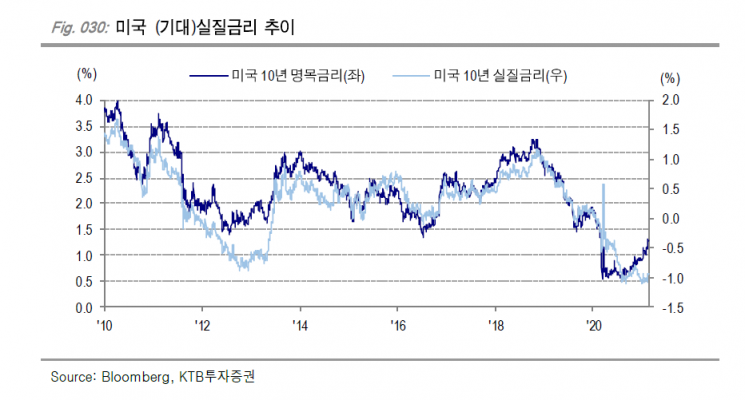

There is an analysis that rising inflation expectations could cause an 'overshooting' (temporary surge) in Treasury yields. This is because the decline in real yields reduces the utility of holding bonds. While nominal yields may rise as a result of policy combinations, from a trading perspective, one-time increases in yield spikes due to trading activities are possible.

Researcher Heo forecasted that yields on the 10-year note should be considered up to 1.50%. Because inflation expectations are high, even if nominal yields reach 1.50%, the real yield level remains accommodative. He also believes the Fed can tolerate a nominal yield rise to around 1.50%. This is based on the judgment that the Fed's high-pressure economic policy is implemented through 'real yield control,' which lowers the expected real yield burden, creating an accommodative funding environment and promoting consumption and investment.

Heo said, "Ultimately, the goal is to fix consumers' inflation expectations upward to raise actual inflation. Considering that the average inflation targeting (AIT) framework has fixed the real yield at -1.0%, nominal yields of 1.50% can be considered a level where overshooting is tolerable."

He emphasized that if overshooting occurs, rather than expecting aggressive Fed intervention and taking it as a buying opportunity at low prices, a wait-and-see approach is necessary. Heo advised, "If the U.S. 10-year yield reaches the 1.50% range due to overshooting, short positions on the 30-year note may shift to the 10-year maturity segment, potentially causing further yield increases. Since position shifts may occur, it is advantageous at this point to reduce duration (average investment recovery period) and focus on short maturities with interest income (carry) strategies."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}