Possibility of Large-Scale Government Bond Issuance Again This Year

Interest in When Bank of Korea Will Respond

Market Says "Will Start Buying Treasury Bonds if 10-Year Yield Exceeds 1.8%"

[Asia Economy Reporter Kim Eun-byeol] As government bond yields continue to rise daily, attention is focused on the Bank of Korea's response. Bond yields are increasing amid expectations that the government will issue a large volume of government bonds again this year to stimulate the economy, but the Bank of Korea has yet to send any significant signals to the market.

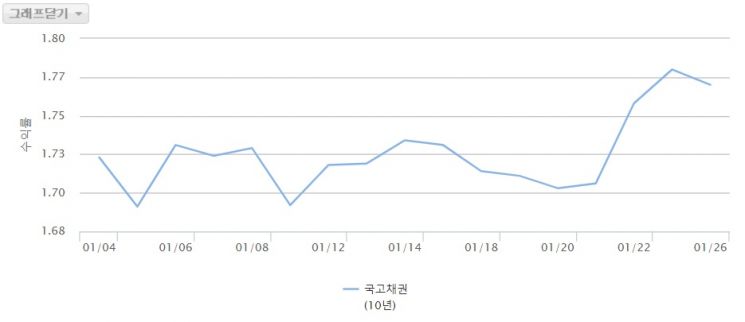

According to the Korea Financial Investment Association on the 27th, the 10-year government bond yield rose to 1.770% the previous day. On the 25th, it even rose to 1.780%, reaching the highest level in one year and two months. The 3-year government bond yield surpassed 1%, rising to 1.007%. Due to expectations of increased bond issuance, prices fell, and yields rose conversely.

Until last year, the market expected the Bank of Korea to intervene and purchase bonds once the 10-year government bond yield reached around 1.5%. This was because a yield level 100 basis points (1bp = 0.01 percentage points) higher than the base interest rate was generally considered high. However, as the Bank of Korea has tolerated yields exceeding 1.5% and 1.75%, the market is now focusing on when the Bank of Korea will take action.

The market views the Bank of Korea's intervention point at 1.8%. A bond market official stated, "Expectations have formed that the Bank of Korea will start purchasing government bonds if the yield exceeds 1.80%."

The Bank of Korea has consistently expressed a principled stance. It has stated that if supply-demand imbalances worsen and long-term interest rate volatility increases, it will actively take measures such as purchasing government bonds or announcing purchase plans. However, it believes the timing of purchases should be determined comprehensively. A Bank of Korea official said, "In the U.S., yields are rising due to the possibility of large-scale economic stimulus following the 'Blue Wave' (Democrats controlling both the House and Senate), so it cannot be simply compared to last year's psychological resistance level (1.5%)."

However, an excessively wide gap between the base interest rate and long-term government bond yields ultimately burdens the Bank of Korea. If long-term yields remain high despite a cut in the base rate, the effects of the rate cut may not materialize. Lower long-term market rates encourage households to increase consumption rather than saving, and companies to borrow money for investment. Unlike household loans, where rates adjust roughly every year (for unsecured loans) or every five years (for mortgage loans), most corporate loans are linked to CD-based variable rates, which could increase interest burdens for companies.

Some argue that the Bank of Korea should directly purchase government bonds in the issuance market, increasing the Bank's burden. Simply put, the Bank of Korea could directly purchase bonds to inject money into targeted areas, but the problem is that such situations could recur. Gong Dong-rak, an economist at Daishin Securities, said, "The recent rise in government bond yields reflects concerns about an unexpectedly large and frequent bond issuance, a supply-demand variable that was not previously considered," adding, "The market is thinking about a change in the fiscal paradigm where the government intervenes whenever there is an issue."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}