Life Insurers' Bancassurance Performance Soars... Up 40.2% Year-on-Year

Banks Also Expand Insurance Product Sales

[Asia Economy Reporter Ki Ha-young] Last year, the bancassurance sales performance of domestic life insurance companies surged significantly. Due to the impact of the novel coronavirus infection (COVID-19), insurance companies strengthened their bancassurance channels, and banks expanded insurance product sales to increase non-interest income.

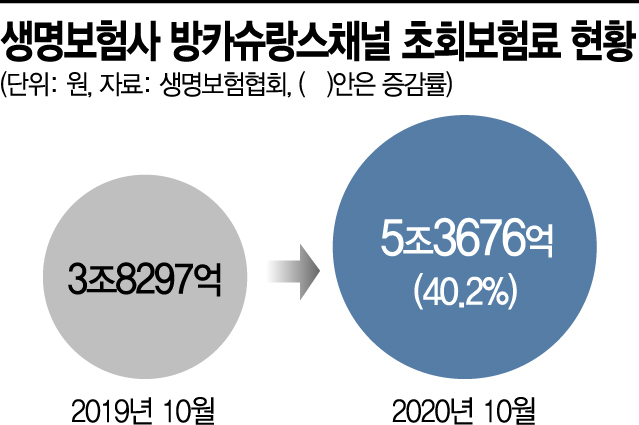

According to the insurance industry on the 25th, the cumulative bancassurance channel first-year premiums of life insurers as of October last year amounted to 5.3676 trillion KRW, a 40.2% increase compared to 3.8297 trillion KRW the previous year. This represents a rapid increase of about 1.5379 trillion KRW within one year.

In particular, the performance of small and medium-sized life insurers stood out. For KDB Life, the amount surged approximately 5676.9% from 2.6 billion KRW the previous year to 150.2 billion KRW during the same period. KB Life also recorded first-year premiums of 157.9 billion KRW through the bancassurance channel during this period, jumping 1004.2% from 14.3 billion KRW in the previous year. Hana Life and DGB Life saw increases of 223.93% and 170.66%, respectively, achieving first-year premiums of 29.996 billion KRW and 5.3 billion KRW.

Large life insurers also performed well. Samsung Life recorded bancassurance first-year premiums of 2.0521 trillion KRW, a 125.8% increase compared to the previous year. This is nearly double, increasing by about 1.1434 trillion KRW from the previous year. Hanwha Life and Kyobo Life also posted increases of 87.5% and 40.5%, respectively, recording 453.1 billion KRW and 183.5 billion KRW.

Alignment of Interests Between Banks Seeking Higher Commission Income

Over the past 2-3 years, life insurers have refrained from selling savings-type insurance products that increase capital volatility in preparation for the introduction of the new International Financial Reporting Standard for insurance contracts (IFRS 17). However, due to difficulties in face-to-face sales caused by COVID-19 last year, they strengthened sales through bancassurance and cyber marketing (CM) channels. For example, KB Life revised its pension insurance product to be exclusively available via mobile bancassurance, resulting in a surge in first-year premiums through the CM channel from 3.1 billion KRW to 9 billion KRW as of October last year.

Banks also increased insurance product sales to expand non-interest income, which analysts say led to a significant rise in bancassurance performance. With fewer customers seeking deposit and savings products due to low interest rates and difficulties in fund sales caused by issues related to incomplete sales of private equity funds, banks increased insurance sales to boost commission income.

The increase in consumers choosing savings-type insurance products with higher interest rates than bank deposits due to low interest rates also had an impact. As the domestic stock market prospered, more consumers sought variable insurance products sold through bancassurance channels that invest part of the premiums in stocks, bonds, and other funds to generate profits. The first-year premiums of variable insurance sold through bancassurance channels reached 1.395 trillion KRW as of the end of October last year, a 40.4% increase from 993.4 billion KRW in the same period the previous year.

An industry insider analyzed, "As the business environment surrounding the financial sector changed due to COVID-19, insurance companies and banks increased insurance sales to secure their respective profits, resulting in a sharp increase in bancassurance performance last year."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}