Banks Apply DSR 40% Regulation on Loans Over 100 Million Won Regardless of Income

Loan Restrictions Even for Non-High Earners... Last-Minute Demand Surge Causes Backlash

Savings Banks Also Raise Funding Bar by Reducing Low-Credit Borrower Handling

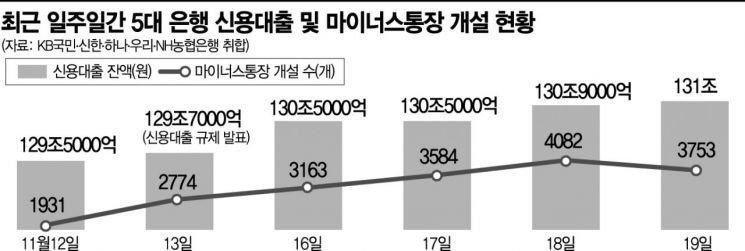

[Asia Economy Reporter Jo Gang-wook] As commercial banks have begun tightening their own credit loans a week earlier than the government’s regulation enforcement date (the 30th), concerns are growing that the 'loan cliff' may become a reality. Initially, financial authorities announced that the loan regulations would target high-income earners, but commercial banks are preemptively applying stricter standards to general credit loans as well. Some banks have even reduced the limits on general salaried worker loans and lowered preferential interest rates. Additionally, savings banks are setting policies not to handle high-interest loans or to recall existing loans ahead of the legal maximum interest rate reduction (from 24% to 20%), raising the funding supply threshold for low-credit borrowers.

Early Credit Loan Regulations Including Reduction of Loan Limits and Preferential Interest Rates

According to the financial sector on the 23rd, major commercial banks have decided to strengthen screening by applying a debt service ratio (DSR) 40% regulation on loans exceeding 100 million KRW regardless of income. KB Kookmin Bank has tightened loan criteria from this day, allowing credit loans only within 200% of annual income. Also, for applicants whose combined credit loans with other banks exceed 100 million KRW regardless of income, the DSR 40% regulation will be applied. The purpose is to curb excessive credit loans relative to income. Woori Bank plans to start early regulation on credit loans exceeding 100 million KRW within this week once related IT system development is completed. NH Nonghyup Bank has started tightening credit loans by reducing loan limits and preferential interest rates.

Regulations Affect Not Only High-Income Earners but Also General Salaried Workers

The issue is that the loan restrictions affect not only high-income professionals but also general salaried workers. Initially, financial authorities described this regulation as a 'pinpoint regulation' to block high-value credit loans for high-income earners. However, in the actual loan market, contrary to the policy intent, it has triggered unexpected last-minute 'excess demand,' leading to stronger banking sector regulations and causing what some call a 'backfire.'

From today, Woori Bank has lowered the maximum limit of 'Woori Main Salaried Worker Loan' and 'Woori WON Salaried Worker Loan' from 200 million KRW to 100 million KRW. Also, the preferential interest rate conditional on salary account, which was 0.2% per annum, has been reduced to 0.1%, and the preferential interest rates for Woori Card usage (over 500,000 KRW every 3 months) and automatic payment of utility and communication bills, which were 0.1%, have been eliminated. NH Nonghyup Bank lowered the maximum preferential interest rate on 'All One Salaried Worker Loan' and 'All One Minus Loan' from 0.5% to 0.3%, a 0.2% point reduction, starting from the 20th. The preferential interest rate conditional on salary account was reduced from 0.2% to 0.1%, and the preferential interest rate for high credit grades (AS grades 1 to 3), which was 0.1%, was completely removed. Hana Bank reduced the maximum limit of 'Hana One Q' credit loan from 220 million KRW to 150 million KRW starting from the 8th of last month, and Shinhan Bank already set the maximum limit for overdraft accounts at 100 million KRW last month.

Suspension of Mortgage Loan Sales... Full-scale Total Volume Management Following Government Warnings

Commercial banks are also drastically reducing the sales of mortgage loans. Following Shinhan Bank and Woori Bank, Hana Bank suspended sales of mortgage loan products such as Gagahoho Mortgage Loan (MCI), One Click Mortgage Loan (MCI), Variable Rate Mortgage Loan (MCG), Mixed Rate Mortgage Loan (MCIㆍMCG), Apartment Loan (MCIㆍMCG), and Fixed Monthly Repayment Mortgage Loan (MCIㆍMCG) starting from the 16th. Additionally, fixed-rate qualified loans will be suspended from the 30th.

Woori Bank, which had suspended MCIㆍMCG loans since the 30th of last month, plans to impose conditional restrictions on 'Woori Jeonse Loan,' a lease deposit loan, until the end of the year. Shinhan Bank had suspended MCIㆍMCG-linked loans but recently resumed them.

Rising Loan Barriers for Low-Income Borrowers with Low Credit

The loan barriers for relatively low-credit, low-income borrowers are also rising. Following the government’s announcement to lower the legal maximum interest rate, savings banks have preemptively reduced handling of low-credit borrowers ahead of the implementation in the second half of next year. Some have even set policies not to issue new loans with interest rates above 20% per annum and to encourage recall of existing loans. According to the Korea Federation of Savings Banks, the proportion of loans exceeding 20% interest among major savings banks with assets around 3 trillion KRW was in the low 20% range as of October, down more than 10 percentage points compared to six months ago. This has raised concerns that vulnerable borrowers such as low-credit and multiple debtors are being pushed out of the formal financial system.

Yoon Chang-hyun, a member of the People Power Party and former head of the Korea Institute of Finance, pointed out, "Experts estimate that the expulsion rate of low-credit borrowers will average 24%, and in some savings banks, it could expand up to 35%."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}