"Insurance Premium Discounts... Do Not Constitute Provision of Special Benefits"

[Asia Economy Reporter Oh Hyung-gil] It is expected that insurance premium discounts will become possible for renewable insurance policies, which reset premiums after a certain period. Renewable insurance policies recalculate premiums every 1, 3, or 5 years, and premiums often increase due to changes in conditions such as age or health status.

According to the insurance industry on the 25th, the Financial Services Commission recently responded that a request for a legal interpretation from an insurance company to operate a 'Membership Credit' program offering premium discounts to policyholders upon contract renewal does not constitute a special benefit.

Renewable insurance policies have lower initial premiums compared to non-renewable policies, which maintain the same premium throughout the payment period. This makes them easier for insurers to sell and preferred by consumers with limited financial resources. A representative product is the renewable indemnity medical insurance, and recently, the types have expanded to include cancer insurance, health insurance, and children's insurance.

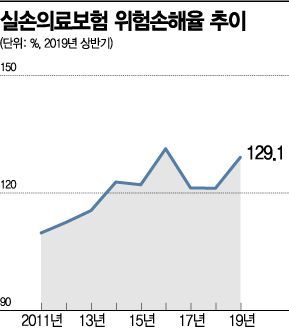

However, after a certain period post-enrollment, premiums tend to become more expensive than non-renewable policies and increase sharply, leading to high consumer dissatisfaction. For example, since standardization in 2009, indemnity insurance premiums rose by about 10% earlier this year. Further premium increases are expected next year due to high loss ratios.

There are cases where renewable insurance is advantageous. It is suitable when the policyholder's premium burden is high or sudden coverage is needed, and it is beneficial for younger age groups due to lower premiums. Renewable insurance is also advantageous if the policy is canceled early or coverage is needed only for a short period.

Premium Discount Conditions Must Be Specifically Stated in Basic Documents

Especially for renewable insurance, it is practically impossible to compare with non-renewable products because future premium increases are uncertain.

As a result, cases of contract cancellations due to difficulty in maintaining contracts are frequently occurring. However, the industry expects that allowing premium discounts for renewable insurance will enhance competitiveness.

The financial authorities have judged that premium discounts must be provided without discrimination to all policyholders and should not be considered as compensation for simple insurance solicitation or inducement benefits.

Under Article 98 of the current Insurance Business Act, persons involved in concluding or soliciting insurance contracts are prohibited from providing or promising special benefits to policyholders or insured persons related to the contract or solicitation. Special benefits include money or premium discounts not based on basic documents, promises to pay insurance benefits exceeding those specified in the basic documents, and premium payments on behalf of the insured.

However, in the case of money, it is allowed to pay the lesser of '10% of the premiums paid during the first year from the contract date' or '30,000 KRW.' Gifts can be provided up to 30,000 KRW for insurance contracts with monthly premiums exceeding 30,000 KRW. Since the 2003 amendment of the Insurance Business Act, this limit has not changed, and there have been calls for its adjustment to reflect current realities.

A financial authority official explained, "Considering that the details of premium discount benefits are reflected in the basic insurance product documents, it may not constitute a special benefit," but added, "Conditions such as discounts or surcharges on insurance benefits must be specifically stated in the basic documents."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}