- New Saeheemang Holssi Supply Amount in the First Half of This Year Decreased Compared to 1.948 Trillion Won in the First Half of Last Year

- First Decrease in Saeheemang Holssi Supply Amount Compared to the Same Period Last Year Since 2015

- Likely Due to Relatively High Interest Rates and Face-to-Face Loan Conditions

[Asia Economy Reporter Park Sun-mi] In the first half of this year, the scale of Saehee-mang Holssi loans, which provide low-interest loans to low-credit and low-income groups, decreased for the first time in five years. This is interpreted as a result of the requirement to visit bank branches in person to obtain the loan, as well as the application of interest rates in the 6-7% range, which are significantly higher than the market loan rates of 1-2%.

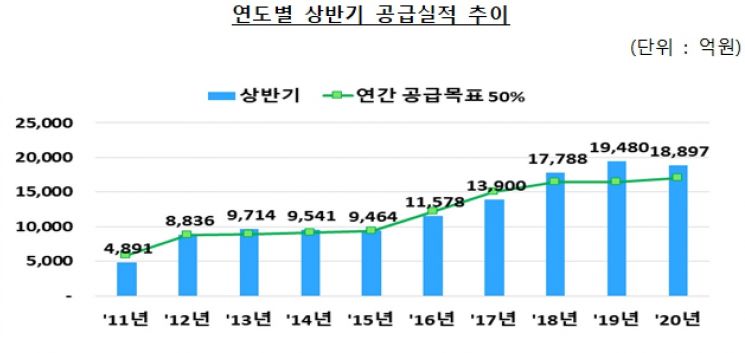

According to the Financial Supervisory Service on the 23rd, the supply performance of Saehee-mang Holssi loans by 15 banks (excluding Industrial Bank and Export-Import Bank) in the first half of this year recorded 1.8897 trillion won (111,844 people). This is a 3% decrease compared to the loan scale of 1.948 trillion won in the same period last year. This is the first time since 2015 that the scale of Saehee-mang Holssi loans has decreased in the first half of the year. However, the Financial Supervisory Service expects no problem in achieving this year’s target, as the loan scale corresponds to 55.6% of the supply target of 3.4 trillion won.

Saehee-mang Holssi is a banking sector financial product for low-income people, lending up to 30 million won (with an interest rate cap of 10.5% per annum) to those with an annual income of 35 million won or less, or those with a credit rating of 6 or lower and an annual income of 45 million won or less. More than 90% of the loans are given to low-credit (credit rating 7 or lower) or low-income individuals (annual income of 30 million won or less).

Saehee-mang Holssi loans have shown explosive response among low-credit and low-income borrowers. The loan scale increased by more than 20% in the first half of 2015-2018 and grew by 9.5% last year. The Financial Supervisory Service adjusted this year’s loan target to 3.4 trillion won, increasing it by 100 billion won from last year, considering the growing demand for Saehee-mang Holssi.

However, the trend has weakened this year. The gap with credit loan interest rates and the COVID-19 situation have had an impact. Although the gap between the average interest rate of Saehee-mang Holssi and household credit loan interest rates is narrowing, reflecting the trend of interest rate cuts, the gap remains large.

Commercial banks are offering various preferential interest rate benefits, resulting in historically low credit loan interest rates in the 1% range, and policy funds such as ultra-low interest loans at 1.5% to support COVID-19 damage are also being supplied. On the other hand, the average interest rate of Saehee-mang Holssi (newly issued loans) in the first half was 6.15%, which is relatively high. This is why demand for Saehee-mang Holssi, with its relatively high interest rates, is decreasing.

The day after the Bank of Korea abruptly cut the base interest rate to a historic low of 0.75% per annum, a bank counter in Seoul appeared quiet on the 17th. Photo by Kim Hyun-min kimhyun81@

The day after the Bank of Korea abruptly cut the base interest rate to a historic low of 0.75% per annum, a bank counter in Seoul appeared quiet on the 17th. Photo by Kim Hyun-min kimhyun81@

Interest Rates Far Higher Than Bank Loans... Face-to-Face Loan Conditions Burdened by COVID-19

The reluctance to visit branches for consultations due to the spread of COVID-19 is also cited as a cause of the demand decrease in the first half. Due to the nature of the product, Saehee-mang Holssi loans are handled through in-person visits to bank branches, where comparisons and recommendations with other products are explained. Visiting a bank branch for low-income financial counseling or making inquiries by phone is a prerequisite. This contrasts with banks releasing non-face-to-face loan products reflecting the COVID-19 situation.

Due to the high interest rates of low-income financial products, the issue is also being discussed in political circles. Lee Jae-myung, Governor of Gyeonggi Province, recently mentioned the basic loan right, arguing that low-credit individuals should also have basic loan rights and that a low-interest, long-term loan system allowing repayment over a long period at low interest rates should be started. However, the Korea Development Institute (KDI) questioned the effectiveness of policy low-income financial products such as Saehee-mang Holssi and Sunshine Loans, stating that simply supplying these products does not reduce users’ high-interest loans like cash advances.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}