- Easier Comparison and Analysis of Bank Products with Open Banking Introduction

- Woori Bank Prepares to Launch Upgraded Real Estate Secured Loan Refinancing Product

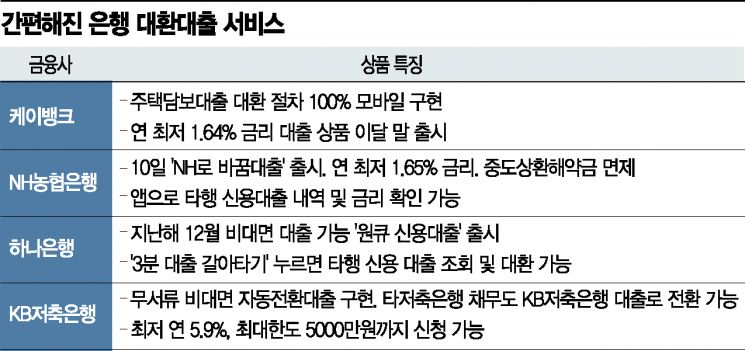

- K Bank Confirms Launch of 100% Non-Face-to-Face Product with Interest Rate as Low as 1.64%

[Asia Economy Reporter Park Sun-mi] With the breakthrough in non-face-to-face applications for refinancing loans (switching loans), an endless competition to poach loan customers between banks has begun. The introduction of open banking (a service that allows transfer and inquiry of other banks' accounts through a single bank application) has made it easier to compare and analyze loan products between banks, so the competition to attract customers is expected to become even fiercer.

According to the financial sector on the 12th, Woori Bank is preparing to launch an updated version of its existing non-face-to-face real estate secured loan product. The key feature is the simplification of the refinancing loan process to enhance customer convenience. The strategy is to encourage customers with real estate secured loans from other banks to switch to Woori Bank using the refinancing loan service. Shinhan Bank is also reviewing systems to launch a non-face-to-face refinancing loan service.

There is already a bank that has confirmed the launch of a 100% non-face-to-face refinancing loan product and declared its intention. K-Bank, an internet-only bank, announced at a press briefing held last week that it will soon introduce a refinancing loan service that can be applied for and processed 100% non-face-to-face. Customers can check the expected loan limit and interest rate without any documents, and spousal and household member consent procedures, as well as delegation procedures required for refinancing, can all be done non-face-to-face. Customers with existing apartment-secured loans can refinance up to 500 million KRW, and apartment-secured loans for living expenses can be refinanced up to 100 million KRW. The interest rate will be applied at the lowest level in the banking sector, starting from an annual rate of 1.64%.

NH Nonghyup Bank has been promoting its refinancing loan application service called 'NH-ro Bakkum Daechul' since this month. It is a mobile-only service that allows customers to easily switch credit loans from other banks to Nonghyup Bank loans. Through the app, customers can instantly check credit loan details, loan limits, and interest rates from multiple banks, and after applying for a loan, switching loans is possible with just one visit to a branch. To drive switching demand, the loan interest rate is set at a minimum of 1.65%, and early repayment penalties are waived.

Savings banks are also actively pioneering the refinancing loan market. KB Savings Bank introduced the 'Kiwi Switching Loan,' a no-document non-face-to-face automatic conversion loan system that converts debts from other savings banks into KB Savings Bank loans. When a customer applies for the Kiwi Switching Loan, KB Savings Bank links with the Credit Information Center database to display refinancing-eligible loans from other companies on the screen. With a single click, the repayment amount is automatically transferred to the virtual account of the respective savings bank.

While there has been competition to attract new loan customers between banks, it is unusual to see product and service competition focused on refinancing loans. As bank loan interest rates have decreased and more people take out loans to invest in real estate and stocks, competition to attract existing loan customers from other banks has emerged. Since banks have offered preferential interest rates to loan customers on the condition of credit cards, salary transfers, and automatic transfers, banks that lose these hard-won loan customers inevitably suffer significant losses. This is why banks are aggressively competing to poach loan customers. If competition for refinancing loans between banks intensifies, the interest rate gap is also likely to narrow further. From the banks' perspective, they need to pay attention not only to simple interest rates but also to other service elements such as convenience.

Meanwhile, industry insiders evaluate that K-Bank, which has no offline branches and has just resumed operations, has pulled the trigger on the non-face-to-face refinancing loan service competition with a 'shut up and attack' strategy. A bank official explained, "Banks are still skeptical about the possibility of 100% non-face-to-face refinancing loans," adding, "In the worst case, banks trying not to lose loan customers might make repayment of existing loans inconvenient by creating obstacles."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}