Financial Services Commission to Lower Bank Personal Business Loan LDR Standards as Early as Mid-Month

Only 85% of Loans Recognized as Lent... Aiming to Ease Soundness Regulations

Banks Secure Additional Capacity for About 70 Trillion KRW in Personal Business Loans

[Asia Economy Reporter Kim Hyo-jin] Starting this month, banks' lending capacity to small business owners will be significantly expanded. This is because financial authorities have relaxed loan-related regulations in response to the novel coronavirus disease (COVID-19).

According to financial authorities on the 2nd, the Financial Services Commission will soon implement a revision to the bank supervision regulations that lowers the loan-to-deposit ratio (loan amount compared to deposits) standard for personal business loans from the current 100% to 85%. This is a follow-up measure to the 'Financial Regulation Flexibility Plan' announced last April in relation to COVID-19 financial support.

The revision will be applied retroactively to personal business loans handled this year. By lowering the loan-to-deposit ratio to 85%, banks need to accumulate fewer deposits for loans, thereby increasing their capacity for new loans. It is expected that this measure will secure additional lending capacity of up to about 70 trillion won.

Personal business loans are mostly provided to small business owners. The financial authorities' policy is to actively supply loans to those whose financial capacity is relatively weak and who have been severely affected by COVID-19. A financial authority official said, "Although not all of the additional capacity will directly translate into loans, it is expected to provide some breathing room."

Yoon Seok-heon, Governor of the Financial Supervisory Service, said at a breakfast meeting with major commercial bank heads this morning, "If COVID-19 prolongs, the management difficulties of small business owners and self-employed individuals may deepen, so attention and support for them are needed more than ever," and urged, "Please make efforts to activate the support system for small business owners and self-employed individuals established in the banking sector so that it can help them."

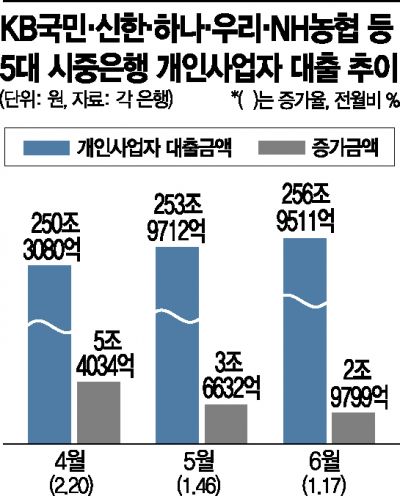

As COVID-19 prolongs, the loan demand from small business owners is expected to continue rising. At the end of last month, the outstanding balance of personal business loans at the five major commercial banks?KB Kookmin, Shinhan, Hana, Woori, and NH Nonghyup?was 256.9511 trillion won, an increase of nearly 3 trillion won compared to May. Although the increase rate slightly decreased compared to the previous month and April, the overall upward trend continues.

An official from a bank said, "Various policy support funds of a short-term nature cannot sustain operations for a long time," adding, "Since the impact of COVID-19 is becoming entrenched, the trend of relying on loans to maintain business operations is expected to continue."

Banks are concerned about potential future credit quality issues. This is because the repayment capacity of small business owners is likely to decline gradually.

Another bank official said, "It is not difficult at all for the authorities to lower regulations and for banks to lend more money," but pointed out, "However, if the supplied loans turn into non-performing loans, the risks to borrowers and the overall financial system will increase in the mid to long term, so it is necessary to consider more macro-level measures."

As of the end of April, the delinquency rate on loans at domestic banks was 0.4%, up 0.01 percentage points from the end of the previous month. The delinquency rate on personal business loans also rose by 0.03 percentage points to 0.36%.

A financial sector official said, "Based on the loss absorption capacity accumulated before COVID-19, banks have been managing to hold on so far and still have some additional absorption capacity," but added, "It is difficult to dismiss concerns because financial distress tends to accumulate invisibly and then suddenly surface."

There are also criticisms that the government's loan maturity extension measures are merely a temporary fix that suppresses the surface manifestation of non-performing loans. Financial authorities are discussing with the financial sector the possibility of extending the loan maturity extension measures, which are currently set to expire in September, by at least three months. Concerns are growing in the financial sector that such measures will only amount to a 'deferral of non-performing loans.'

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}