Impact of 5 Consecutive Months of COFIX Decline

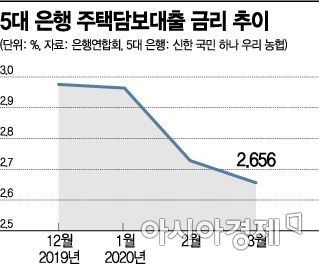

Average of 2.656% for 5 Major Banks in March

NH Nonghyup Lowest at 2.27~3.88% Annually

[Asia Economy Reporter Kim Min-young] Bank mortgage loan interest rates have fallen to historically low levels. This is due to the decline in COFIX (Cost of Funds Index), which serves as the benchmark for variable mortgage loan rates in the banking sector. Financial consumers preparing to take out loans are now faced with the dilemma of choosing between variable and fixed rates.

According to the financial sector on the 18th, the newly issued COFIX based on new transaction amounts last month was 1.20%, down 0.06 percentage points from March. This marks a decline for five consecutive months. The new balance-based COFIX also fell to 1.31%, down 0.07 percentage points from March. It has been declining for 10 months since its first announcement in July last year. COFIX is the weighted average interest rate of deposit products through which domestic banks raise funds. Simply put, since banks borrowed money from financial consumers at a lower cost, loan interest rates have also become cheaper accordingly.

Mortgage loan interest rates linked to COFIX also dropped across the board. Starting today, NH Nonghyup Bank applied mortgage loan rates based on the new COFIX at an annual rate of 2.27% to 3.88%, the lowest among the five major banks.

Kookmin Bank offers 2.40% to 3.90%, Woori Bank 2.71% to 4.31%, Hana Bank 2.740% to 4.040%, all at historically low levels. Shinhan Bank also adjusted rates to 2.49% to 3.74%. Although slightly higher than the record low on the 20th of last month (2.45% to 3.46%), the rates remain low.

Mortgage loans based on the new balance also fell to historically low levels at all five major banks. The average among the five banks ranges from a minimum of 2.38% to a maximum of 4.42%.

Mixed (fixed) rates are also forming a 'bottom.' The mixed rate is based on the 5-year financial bond rate. Kookmin Bank offers the lowest at 2.13% to 3.63%, followed by Nonghyup Bank at 2.17% to 3.58%, Hana Bank at 2.309% to 3.609%, Shinhan Bank at 2.60% to 3.61%, and Woori Bank at 2.72% to 4.13%.

Mortgage loans actually handled at branches also recorded historically low interest rates. According to the Bankers Association, the average interest rate for loans issued in March (mortgage loans with a maturity of 10 years or more and installment repayment method) among the five major banks was 2.656%.

Even if a borrower takes out a 300 million KRW loan from a bank, the annual interest is only about 8 million KRW, which amounts to approximately 670,000 KRW per month.

Prospective homebuyers are calculating which loan option is more advantageous. Fixed rates are still generally cheaper for now, but based on the lowest interest rates, a 'rate inversion phenomenon' has even appeared where variable rates are lower than fixed rates. Additionally, depending on individual customers' income, loan conditions, and preferential rates, variable rates may be more favorable. A financial sector official said, "If the ultra-low interest rate trend continues for the next few years, variable rates are much more advantageous," adding, "If you do not want to worry about interest rate fluctuations, using fixed rates is also a good option."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![User Who Sold Erroneously Deposited Bitcoins to Repay Debt and Fund Entertainment... What Did the Supreme Court Decide in 2021? [Legal Issue Check]](https://cwcontent.asiae.co.kr/asiaresize/183/2026020910431234020_1770601391.png)

{kind=link}