Government Issues Successive High-Intensity Loan Regulations... Brokerage Offices Also Facilitate to Evade Restrictions

[Asia Economy Reporter Lee Chun-hee] Despite the government’s repeated tightening of financial channels to block idle funds from flowing into the housing market, it has been revealed that P2P (Peer to Peer) mortgage loans exceeding the Loan-to-Value (LTV) ratio limits are still being made in various parts of Seoul. Although the government declared it would strongly block even indirect loans when it announced the December 16 real estate measures last year, the field still shows a balloon effect of loans circumventing regulations.

According to the industry on the 22nd, even after the government’s policy announcement, major P2P lending companies continue to promote products with phrases such as “Loans available up to 2 billion KRW with LTV 85% and no application of Debt Service Ratio (DSR),” and “Higher limits and faster, more convenient loans than financial institutions.” It is also easy to find related flyers from well-known P2P lenders at frontline real estate agencies. In real estate communities where market participants exchange information, inquiries about P2P real estate-backed loans have been frequently posted as conventional loans become restricted.

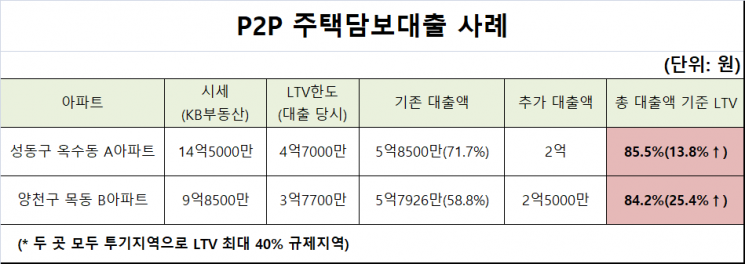

In fact, some P2P loans have been confirmed to have been made at up to 85% of the property value even after the government’s policy announcement. An apartment in Oksu-dong, Seongdong-gu, Seoul, with a market price of 1.45 billion KRW, currently allows loans up to only 470 million KRW. This is because LTV regulations of up to 40% apply to amounts under 900 million KRW and up to 20% for amounts exceeding 900 million KRW in speculative areas. However, the total mortgage loan amount on this apartment has reached 85% of the market price. This is due to indirect loans through insurance loans amounting to 1.04 billion KRW already taken, as well as an additional 200 million KRW P2P loan made on the 8th. Similarly, in an apartment in Mok-dong, Yangcheon-gu, where the 40% LTV regulation has been applied since August last year, a 250 million KRW P2P loan was made, raising the total mortgage loan amount to 829.26 million KRW, which is 84% of the market price of 950 million KRW.

The continuation of P2P loans despite much higher interest rates than bank mortgage loans appears to be due to investors whose funding routes have been blocked by the government’s high-intensity loan regulations flocking to P2P lending. According to data from the Korea P2P Finance Association surveying loan status of 45 member companies, the outstanding balance of real estate-backed loans reached 561.8 billion KRW at the end of last year. This is a 57% increase from 358.3 billion KRW at the end of 2018. In particular, individual real estate-backed loans nearly doubled from 169.3 billion KRW at the end of 2018 to 332.9 billion KRW at the end of last year.

The problem lies in the lack of means to regulate P2P loans. Last month, the P2P industry announced restrictions such as “a complete ban on loans for ultra-high-priced homes over 1.5 billion KRW” and “loan restrictions on high-priced homes over 900 million KRW if there is a possibility of using the loan for home purchase funds,” but there are no regulations on LTV. Although the “Online Investment-Linked Finance Business and User Protection Act,” which includes regulations on P2P lending, has been enacted, it is scheduled to be implemented only in August. The financial authorities are reportedly considering adding regulations on mortgage loan LTV during the current process of drafting related enforcement ordinances.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}