Shift toward "large-scale, long-term, performance-oriented" mandates expected

"Funds must be managed independently, centered on private-sector experts"

Clarifying responsibility and building trust will be key to embedding the scheme

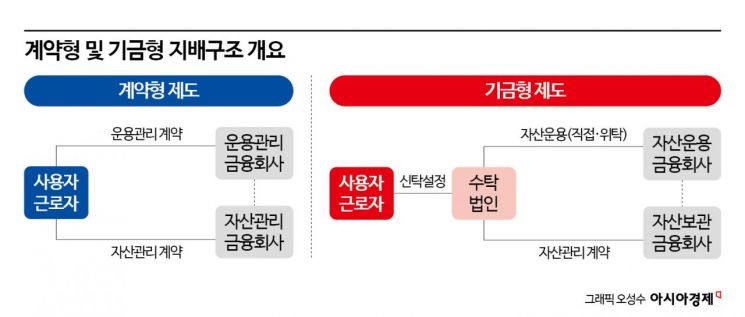

With the introduction of the "fund-type" scheme alongside the existing contract-type structure in the domestic retirement pension market, significant changes are expected across the financial investment industry. As competition over large-scale, long-term capital intensifies in earnest, expectations are growing that new opportunities will open up for the asset management industry. At the same time, some point out that, in order to enhance the effectiveness of the system, it is necessary to clarify the responsibility structure and governance of fund management, and to introduce support measures that take into account the burden on companies and employees.

"Seize the opportunity"...Asset management competition to begin in earnest

According to the financial investment industry on the 11th, market participants expect that the introduction of the fund-type retirement pension scheme will trigger a restructuring of retirement pension management demand toward "large-scale, long-term, and performance-oriented" mandates.

Asset management companies, which have so far competed on the basis of individual products under the existing contract-type framework, will be able to take part in competition to manage assets on a fund-unit discretionary basis going forward, and their role in the market is expected to grow significantly. In addition, as bidding competition in the process of selecting fund trustee corporations and an entrusted management structure take hold, investment capabilities and track records are expected to emerge as key competitive factors, going beyond simple product competition. If various fund models such as open-architecture funds operated by financial institutions and joint funds are allowed, asset allocation strategies and long-term management capabilities tailored to each model will inevitably be required. An industry insider, referred to as Mr. A, predicted, "Competition driven by short-term performance and marketing will ease, and we will see management competition from a medium- to long-term perspective, including asset allocation and risk management aimed at medium- to long-term performance."

In particular, if capital is pooled into large funds, there will be more room to pursue long-term investment strategies based on economies of scale, such as expanding exposure to private equity, alternative investments, and overseas assets. This is the backdrop to the market’s interpretation of the latest decision as a signal of a structural shift in retirement pension management demand toward a "large-scale, long-term, and performance-oriented" model. Even at the beginning of the year, preemptive moves to prepare for the introduction of the fund-type scheme were already visible in the industry, such as Hanwha Asset Management establishing a dedicated retirement pension business division.

However, despite the various opportunity factors, it is still unclear who will actually become the main fund management entities and what impact the change will have on individual plan participants. Another asset management industry insider, referred to as Mr. B, said, "As retirement pensions are converted into funds, trustee corporations will be established and companies will contribute money to them," adding, "It is certainly a new opportunity, but since no concrete blueprint has been presented, we still do not know whether securities companies will have an advantage or asset management companies will have an advantage." Concerns cited include the burden of expanding organizations and staffing in preparation for fund conversion, and the possibility that the investment autonomy of firms that fail to become fund managers could be restricted.

"The key questions are who and how"...Direction of policy design

Experts assess that the latest agreement has opened up the possibility of transforming the retirement pension management structure by preserving participant choice while allowing various fund-type models such as open-architecture and joint funds. Youngjoo Nielsen, CEO of Korea Retirement Pension Data and professor at Sungkyunkwan University SKK GSB, said, "This is a meaningful first step toward a substantial transformation of the retirement pension system," and added, "It is positive in that it incorporates both the participation of private financial institutions and a structure that preserves participant choice."

However, many point out that the success or failure of the scheme will depend on the details of policy design going forward. Above all, the core task is seen as building a trustworthy fund governance structure and securing participant confidence through information provision and decision-making support systems. Nielsen stressed, "Simply granting choice is not enough," and added, "We need a structure that transparently discloses the design, performance, and risks of the funds and helps participants understand them." In a report published last year, Nam Jaewoo, Head of the Fund and Pension Division at the Korea Capital Market Institute, cited the example of Australia’s superannuation system and evaluated that "fund-type governance is an institutional mechanism that enhances management efficiency from a risk-adjusted return perspective, rather than simply pursuing high returns."

A recurring issue in overseas examples, including Japan, has been the responsibility structure in the event of investment underperformance. If the responsible parties and loss-sharing arrangements are unclear, trust in the system may be undermined. There is also a possibility that participants will avoid choosing funds altogether, or that a pattern of avoiding responsibility for poor performance, similar to what was seen when default options were introduced in the past, will re-emerge. In addition, given the currently low adoption rate, some warn that if mandatory participation and expansion of the fund-type scheme get ahead of actual practice, companies on the ground may perceive it as yet another regulation. Accordingly, some argue that, rather than imposing a uniform mandate, a step-by-step approach is needed to expand participation through incentives such as tax benefits and reductions in administrative burdens.

Nielsen suggested, "Even if the fund-type scheme is introduced, reality may not change if institutional safeguards are not put in place," and added, "A clearly defined decision-making process, and a structure that grants legal immunity when that process is followed, must be implemented in parallel."

In particular, for the fund-type retirement pension scheme to take root over the long term, it will be necessary to establish an independent management framework centered on private-sector experts and to introduce institutional safeguards that prevent the funds from being used for policy purposes or as tools to prop up the stock market.

Nam noted, "Along with strengthening supervisory capabilities over fund trustee corporations, it will be necessary to mandate the participation of external experts on the boards of nonprofit trustee corporations, and for for-profit trustee corporations, institutional mechanisms must be established to protect employees’ benefit entitlements in the event of fund bankruptcy." He added that, for funds operated under a CDC (collective defined contribution/defined benefit hybrid) structure, measures to guarantee a minimum level of return should also be considered.

Some in the market are also watching whether the National Pension Service will participate. On this point, an official from the financial authorities drew a line, saying, "Given that the fund-type retirement pension scheme has not yet been fully established institutionally, it may be premature to discuss National Pension participation at this stage."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}