Secondary Financial Sector Faces High PF Project Exposure Amid Real Estate Slump

Continued Oversight Needed, Including Additional Provisions at Savings Banks

As construction companies continue to collapse one after another due to the severe slump in the real estate market, an analysis has emerged suggesting that the risk of real estate project financing (PF) defaults in the secondary financial sector?including savings banks, securities firms, and capital companies?may increase in the future.

According to financial authorities and Korea Ratings Corporation (Korea Ratings) on the 6th, the outstanding balance of real estate main PF in the domestic secondary financial sector was approximately KRW 44.6 trillion as of December last year, accounting for about 29.5% of the total main PF in the financial sector. Although the proportion is not high overall, unlike the primary financial sector, the secondary financial sector has a higher proportion of real estate PF in its asset composition, which is why it is classified as risky.

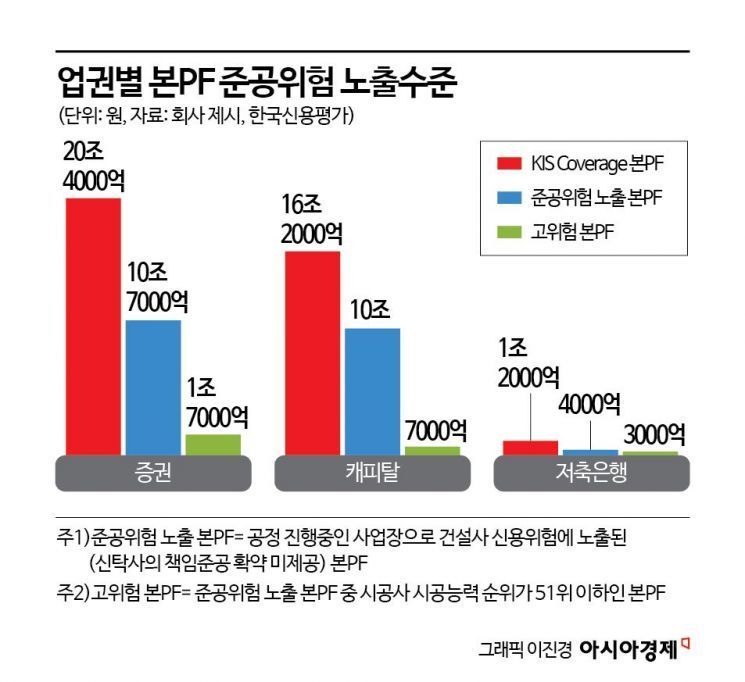

Secondary Financial Sector’s Risk Exposure Reaches KRW 21.2 Trillion

Korea Ratings estimates the construction company risk exposure in the domestic secondary financial sector to be about KRW 21.2 trillion, based on main PF projects currently underway. Among this, exposure to large construction companies ranked 1st to 20th in construction capability evaluation is KRW 15 trillion, exposure to mid-sized construction companies ranked 21st to 50th is KRW 3.6 trillion, and exposure to small and medium-sized construction companies ranked below 51st is approximately KRW 2.7 trillion.

While the likelihood of problems arising from highly creditworthy large construction companies is low, it is pointed out that mid-sized and small construction companies should be carefully monitored given the recent sluggish real estate market conditions.

According to the Korea Construction Industry Research Institute, the number of closure reports by general construction companies last year reached 641, a 10.3% increase compared to the previous year. This is the highest since the survey began in 2005 (629 cases), and most of the closed construction companies were small and medium-sized firms. Construction company closures are continuing this year as well. On the 6th of last month, Shindonga Construction, a mid-sized construction company ranked 58th in construction capability, filed for court receivership, and on the 19th, Daejeo Construction, the second-largest construction company in the Gyeongnam region (ranked 103rd), also filed for court management.

The situation of local small and medium-sized construction companies like Daejeo Construction is assessed by the industry to be worse than it appears on the surface. A Korea Ratings official stated, "Considering the sluggish local real estate market and ongoing cost burdens, it is estimated that a significant number of small and medium-sized construction companies are exposed to liquidity risks," adding, "The actual level of default risk for small and medium-sized construction companies is likely higher than the financial levels shown in their financial statements."

He continued, "In the case of mid-sized construction companies, the likelihood of credit risk materializing is relatively low compared to small and medium-sized companies," but emphasized, "Given the average exposure per individual company reaching KRW 200 billion, the impact on the market could be significant if credit risk occurs, so managing default risk is necessary."

As Construction Company Defaults Increase, Secondary Financial Sector Risks Also Rise

As defaults among construction companies increase, the possibility of risk transmission to the financial market, centered on the secondary financial sector, also grows. Among the secondary financial sector, savings banks have relatively high exposure to real estate PF risks.

Although the high-risk main PF balance of savings banks is about KRW 300 billion, which is not large in scale, unlike other secondary financial companies, construction companies with lower construction capability rankings mainly participate as contractors. The high-risk main PF balance for securities firms is KRW 1.7 trillion, and for capital companies, it is KRW 700 billion.

A Korea Ratings official evaluated, "In the case of securities and capital companies, more than 70% of the construction companies involved have excellent construction capabilities, but in the case of savings banks, many contractors are construction companies with inferior construction capabilities, resulting in higher exposure to completion risk."

In fact, the Financial Supervisory Service recently conducted on-site inspections targeting savings banks where real estate PF default risks are a concern, and requested additional provisioning from some of them. It is understood that savings banks with many non-performing assets below the fixed asset level were ordered to accumulate more provisions than the set standards. The delinquency rates for construction and real estate loans in the non-bank sector (based on principal and interest overdue by one month or more) were 8.94% and 6.85%, respectively, as of the third quarter last year, the highest in nine years and six months.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}