Proportion of Interest Income in Domestic Banks' Total Profits Reaches 88.6% as of Q3 Last Year

Most Interest Income Comes from Loans, Loan Interest Remains Core of Bank Profits

Economic Structural Changes Expose Limits of Interest-Based Banking, Necessitating Strategic Shift

As domestic banks are posting record profits through interest income from loans, concerns have been raised that the future of loan business is becoming uncertain due to changes in the economic structure, necessitating a fundamental shift in business strategies.

Banks' Interest Income Proportion Too High, Facing Limits Soon Due to Economic Structural Changes

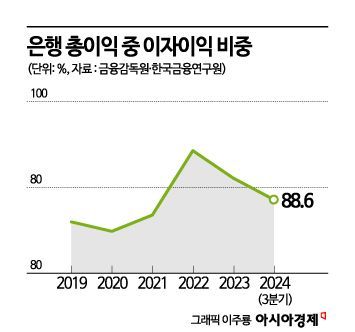

According to the Korea Institute of Finance on the 3rd, the proportion of interest income in the total profits of domestic banks reached 88.6% as of the third quarter of last year, with most of it coming from loan interest. The proportion of interest income in domestic banks peaked at 94% in 2022 and has slightly decreased since, but it still remains the core business model accounting for the majority of bank profits. The loan-to-total-assets ratio of domestic banks has steadily increased since it first exceeded 50% in 2002, reaching 61.5% in the third quarter of last year.

The institute analyzed that as the domestic economic structure rapidly changes, the business model of domestic banks, which mainly generate profits from loan interest, will soon face limitations.

First, it pointed out that Korea's real economy, which forms the foundation of bank loans, is expected to grow at a low rate of around 1%, which is unfavorable for a loan-centered profit strategy. Korea's average annual economic growth rate was 9.4% before the 1997 financial crisis but has steadily declined to about 2.0% after the COVID-19 pandemic. Without productivity improvements such as structural reforms, Korea's potential growth rate is expected to fall to 0.6?0.7% by the 2040s, indicating unfavorable economic conditions for banks' loan businesses.

Population decline and aging are also expected to limit banks' household loan-focused profit strategies. Korea's population peaked at 51.8 million in 2020 and is projected to fall below 50 million by 2041. As the population decreases, basic loan demand will naturally decline. The proportion of elderly population (aged 65 and over) exceeded 15% in 2020 and is expected to surpass 30% by 2036. As aging progresses, loan demand that involves borrowing against future income will also decrease.

Falling interest rates are also negative for banks' loan businesses. If the low-growth phase continues, market interest rates will remain low, leading to a decline in net interest margins, which are the profitability of loans. This will reduce the attractiveness of loans in banks' businesses, the institute diagnosed. Additionally, with low economic growth and the gradual development of capital markets, it will be difficult for corporate loan demand to increase significantly, which is also unfavorable for banks' loan businesses.

Active Expansion of Non-Interest Income and Overseas Expansion Needed

The institute emphasized that banks must recognize the significantly reduced sustainability of loan-centered profit strategies in the future and actively pursue fundamental strategic changes such as increasing non-interest income, expanding businesses like trusts and asset management to prepare for population aging, and expanding overseas operations into countries with higher growth rates and younger populations.

Lee Byung-yoon, Senior Research Fellow at the Korea Institute of Finance, stated, "Increasing non-interest income should be understood not merely as a way to reduce the proportion of interest income, which is highly volatile due to economic fluctuations, to secure stable profits, but as a strategic change to prepare for a reduction in interest income caused by declining loan demand in the future."

He added, "Efforts to increase non-interest income through enhancing fee income, revitalizing venture investments, and expanding accounting, management consulting, and advisory services for small and medium-sized enterprises are necessary. Expanding trust and asset management businesses to prepare for population aging will also contribute to increasing non-interest income. Institutional improvements by financial authorities are also needed for this." Furthermore, he explained, "Expanding overseas operations mainly in countries with lower average ages and higher growth rates should be understood as an essential strategy, not an option, in terms of creating new sources of bank revenue."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}