Preparation of Comprehensive Summary Table Format... Terminology Standardization

Mandatory Entry of Current Exposure and Maximum Exposure

As concerns over domestic real estate project financing (PF) have grown following Taeyoung Construction's workout (corporate restructuring) application, financial authorities have decided to revise the previously inconsistent disclosure system.

On the 2nd, the Financial Supervisory Service (FSS) announced that it has prepared a model case for note disclosures on contingent liabilities related to construction contracts of construction companies.

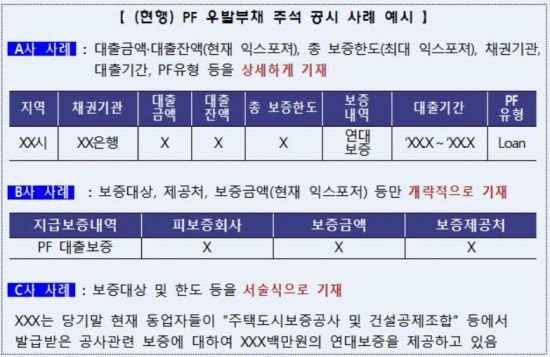

First, a comprehensive summary table format was created to easily identify the scale of contingent liabilities and the maturity-based exposure of underlying assets such as loan claims by real estate PF project stage or type. To facilitate comparison, terminology was standardized, and essential items such as current exposure (guarantee amount) and maximum exposure (guarantee limit) were also presented.

Currently, the concept of current exposure is mixed with guarantee amount, executed amount, loan amount, and loan balance. Maximum exposure is also used interchangeably with contract amount and guarantee limit. There are cases where only part of the current exposure or maximum exposure is disclosed.

Maturity information was also subdivided by separately classifying amounts due within 3 months and 6 months. This reflects the fact that many securitized bonds such as asset-backed commercial paper (PFABCP) and asset-backed (AB) short-term bonds have maturities of 3 or 6 months.

Risk levels are also reflected. By project entity, it is divided into redevelopment projects and other projects, and by project stage, into bridge loans and main PF loans. In cases where multiple credit enhancements are provided for a single PF loan, the comprehensive summary table requires the amount excluding overlapping parts to capture the total exposure.

For consortium projects, the guarantee limit of the consortium and the company's burden ratio must be disclosed to assess the company's risk exposure. However, to reduce disclosure burden, projects with guarantee amounts less than 1% of the total real estate PF guarantee amount or under 10 billion KRW may be collectively listed as "Others" without separate classification.

Credit enhancements for relatively lower-risk interim payment loans and social overhead capital (SOC) projects are required to disclose only a summary table showing the total amount without detailed breakdowns.

The FSS will conduct a field inspection to verify whether contingent liabilities have been faithfully disclosed in the notes once the 2023 financial statements of listed construction companies are published. Additionally, it plans to guide the "model case for note disclosures" through organizations such as the Korea Listed Companies Association and incorporate it into the "Corporate Disclosure Form Preparation Standards."

The FSS stated, "With the announcement of the model case for note disclosures on contingent liabilities related to construction contracts, it is expected that real estate PF contingent liabilities of construction companies will be disclosed more systematically and consistently. We will encourage the faithful recording of necessary information for information users to enhance the evaluation and comparability of construction companies' risk levels."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}