June 22 Federation of Korean Industries Survey Released

2011: 14.4% → 2021: 21.6%

Sovereign → SK Elliott → Hyundai Motor Attacks

Activist Funds' Management Takeover Followed by 'Exit'

"Support Owner Defense Rights like Dual-Class Voting

to Overcome the 'Tilted Playing Field'"

Paul Singer, the founder of Elliott, a US-based activist private equity fund that aimed for management rights of Hyundai Motor Group. (Photo by Asia Economy DB)

Paul Singer, the founder of Elliott, a US-based activist private equity fund that aimed for management rights of Hyundai Motor Group. (Photo by Asia Economy DB)

[Asia Economy Reporter Moon Chaeseok]

#The hedge fund Sovereign Fund purchased 14.99% of SK Inc., the holding company of SK Group, in April 2003. To avoid the 3% voting rights restriction during the election of audit committee members, it preemptively distributed 2.99% stakes to five subsidiaries in a 'share splitting' strategy. Meanwhile, it made demands such as the resignation of the existing management, opposition to support for underperforming affiliates, and increased dividends. SK Group had no choice but to spend about 1 trillion KRW to defend its management rights. Two years later, Sovereign exited after earning 945.9 billion KRW, five times its investment, through stock trading gains and dividends. This is what is commonly called a 'muk-twi' (eat-and-run) case.

#The US-based activist private equity fund Elliott Management attacked Hyundai Motor Group and Samsung Group. In particular, Elliott targeted Hyundai Motor Group’s governance and dividends, proposing a dividend of 21,967 KRW per share in early 2019, among other shareholder proposals. This was an unreasonable demand, with a year-end dividend of 5.8 trillion KRW and a payout ratio of 387%, exceeding three times Hyundai Motor’s 2018 net profit of 1.645 trillion KRW. Investors sided with Hyundai Motor, but significant turmoil could not be avoided. This also became an opportunity for activist funds like KCGI to emerge domestically.

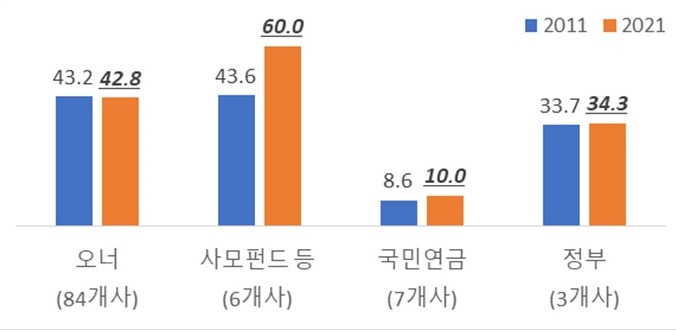

Changes in the shareholdings of major shareholders holding 5% or more stakes in the top 100 asset companies. (Data=Federation of Korean Industries)

Changes in the shareholdings of major shareholders holding 5% or more stakes in the top 100 asset companies. (Data=Federation of Korean Industries)

On the 22nd, the Federation of Korean Industries (FKI) announced that last year, compared to 10 years ago, the shareholding of private equity funds in the top 100 companies by assets increased by more than 7 percentage points, while owner shareholdings decreased. Since activist funds, which make unreasonable demands such as dividends or governance restructuring and then realize gains, are mixed among private equity funds, the means for corporate owners to defend management rights are insufficient, highlighting the urgent need for institutional reforms such as the introduction of 'dual-class voting rights.'

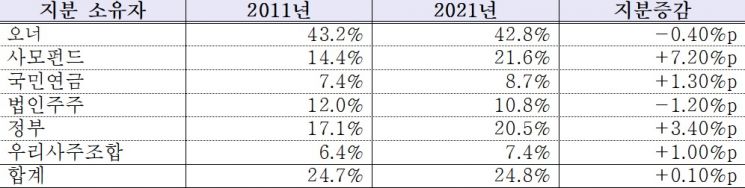

According to the 'Survey on Changes in Major Shareholders’ Stakes in the Top 100 Companies by Assets from 2011 to 2021' released by FKI on the same day, the average shareholding of private equity funds among major shareholders holding more than 5% in the top 100 companies increased from 14.4% in 2011 to 21.6% last year, a rise of 7.2 percentage points. In comparison, the National Pension Service’s shareholding rose by 1.3 percentage points (7.4% → 8.7%), and owners’ shareholding fell by 0.4 percentage points (43.2% → 42.8%), making the presence of private equity funds noticeably larger.

Average Shareholding Changes of Major Shareholders from 2011 to 2021. (Source: Federation of Korean Industries)

Average Shareholding Changes of Major Shareholders from 2011 to 2021. (Source: Federation of Korean Industries)

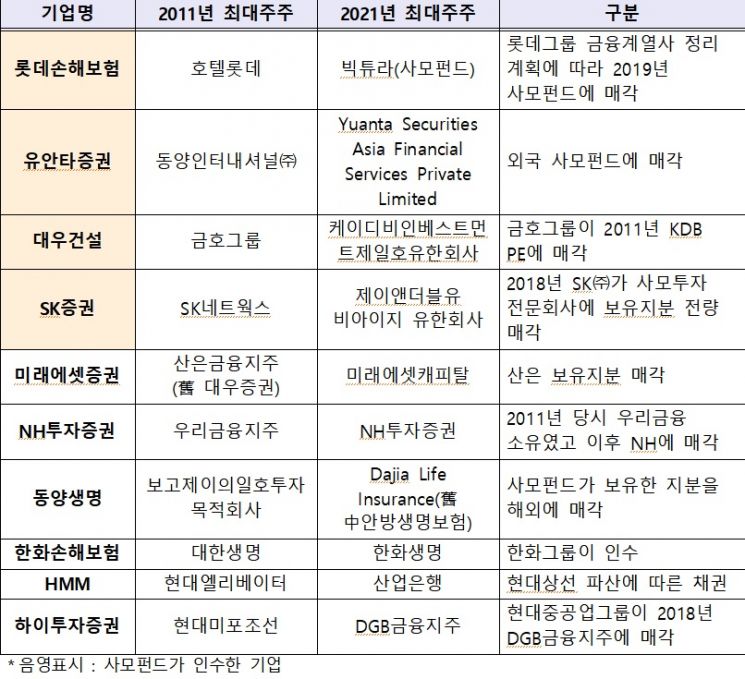

FKI pointed out that as the government promotes the participation of stakeholders such as private equity funds and the National Pension Service in corporate management by revising the Capital Markets Act and the Commercial Act, the increase in private equity fund shareholdings has triggered an emergency in corporate management rights defense. In fact, among the 100 companies surveyed over 10 years, private equity funds acquired management rights in 4 companies, including Lotte Insurance, Yuanta Securities, Daewoo Construction, and SK Securities.

The problem is that private equity funds, as financial investors, are initially friendly to management but later threaten management rights under the pretext of shareholder agreements. A recent example is the dispute between Kyobo Life Insurance and the Affinity Consortium. From the corporate perspective, the risk of management rights takeover outweighs the positive functions of private equity funds, such as acquiring financial affiliates necessary for conversion to holding companies or injecting funds to overcome temporary liquidity crises.

There are also criticisms that government policies, such as abolishing the '10% ownership obligation' under the Capital Markets Act to foster domestic private equity funds, are adversely affecting corporate management rights. Elliott’s precedent of making huge capital gains by blocking Hyundai Motor Group’s governance plan in 2019 and opposing the Samsung C&T-Cheil Industries merger in 2015 is cited, and FKI argues there is no guarantee that domestic private equity funds will not attack management rights like Elliott.

Conversely, corporate owners lack sufficient means to defend management rights. FKI pointed out that the '3% rule,' a voting rights restriction guaranteed by the Commercial Act, severely burdens the largest shareholders in competition with other major shareholders. As confirmed in the 2003 management rights dispute between Sovereign and SK, the largest shareholder can only exercise voting rights up to 3% even when combined with related parties, but hedge funds or private equity funds can exercise voting rights for their entire holdings through 'share splitting.' This involves acquiring stakes of 2.99% in multiple subsidiaries and then engaging in vote battles at shareholders’ meetings.

Yoo Hwan-ik, head of the Industry Division at FKI, said, "The government is encouraging the participation of the National Pension Service and private equity funds in corporate management by revising the Enforcement Decree of the Capital Markets Act, but it is ignoring corporate opinions that call for management rights defense measures such as dual-class voting rights." He emphasized, "Institutional improvements are urgently needed so that management rights attackers and defenders can compete equally in the management rights market."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}

{kind=link}