Financial Sector Bills Total 169 Trillion Won... Debt Bills as 'Time Bomb'

Populist Financial Policies Likely to Distort Market

Despite Criticism of Contradicting Market Logic, Some Legislation Enacted

[Asia Economy Reporters Kiho Sung and Seungseop Song] It has been revealed that last year, the amount mobilized by the five major financial holding companies in relation to COVID-19 reached 168.7 trillion won. This was the result of pressure from the government and political circles on financial companies under the pretext of supporting low-income financial services. While demanding financial soundness management such as refraining from dividends in preparation for a prolonged economic recession, there is criticism that the demand to hand over profits earned is contradictory.

According to the financial sector on the 11th, despite the COVID-19 crisis last year, the five major financial holding companies?KB, Shinhan, Hana, Woori, and NH Nonghyup?recorded a net profit of 12.5502 trillion won in the first quarter of this year. Most of the financial holding companies that posted record-breaking performances last year continued their achievements with all-time high records this year as well. However, the mood among financial holding companies is not bright. With the upcoming by-elections this year and the presidential election next year marking the start of a full-fledged election season, there is a possibility that the level of demands from the government or political circles will increase.

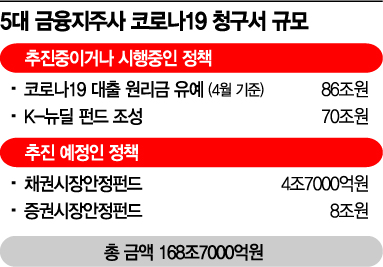

From April last year to the end of April this year, the principal deferment scale of COVID-19 loans by the five major banks?KB Kookmin, Shinhan, Hana, Woori, and NH Nonghyup?was 86 trillion won (350,000 cases). The five major financial holding companies announced a support plan of about 70 trillion won for the K-New Deal Fund, which is being promoted by the government. In addition, the amendment to the Low-Income Financial Support Act, which collects 100 billion won annually from financial companies to support low-income financial services and is evaluated as a 'financial sector profit-sharing system,' was passed in March this year without significant opposition from either party.

Despite the large-scale formation, a considerable amount remains unused. In the case of the Bond Market Stabilization Fund, launched last year with a goal of raising 20 trillion won, the amount allocated to banks was 4.7 trillion won. The Securities Market Stabilization Fund, aimed at raising 10 trillion won, also planned for 8 trillion won to be shared by the five major financial holding companies and large securities firms outside of them. Both funds can be reactivated anytime if the bond and stock market conditions worsen. Adding up the COVID-19 financial support amount, the K-New Deal Fund, and the Bond and Securities Stabilization Funds, the total reaches a staggering 168.7 trillion won.

The financial sector agrees that financial companies should cooperate during economic difficulties but warns that excessive shifting of responsibilities that the government should bear onto financial companies could lead to insolvency. In fact, financial-related bills in the political arena have accelerated since the start of the 21st National Assembly, mainly led by the ruling Democratic Party. Populist bills such as lowering the legal maximum interest rate, bank debt forgiveness laws, interest suspension laws, profit-sharing systems, as well as various regulatory legislations like punitive damages and amendments to the Insurance Business Act known as the Samsung Life Act, are being pushed or discussed.

The Moon Jae-in administration has been implementing these measures under the pretext of protecting low-income groups despite criticisms that they contradict market logic. A representative example is the reduction of the legal maximum interest rate. The legal maximum interest rate will be lowered from 24% to 20% annually starting July 7. The legal maximum interest rate, which was lowered from 39% in 2011 to 34.9%, then to 27.9% in 2016, and 24% in 2018, was promised by candidates in the 2017 presidential election to be lowered to 20% and was enacted accordingly. Initially, financial authorities opposed this, citing concerns that some low-credit borrowers might be pushed to illegal private loans due to inability to obtain loans from financial companies, but they eventually yielded to political pressure. Additionally, Gyeonggi Province Governor Lee Jae-myung proposed last year to lower the legal maximum interest rate to around 10%, and Democratic Party lawmaker Kim Nam-guk also introduced related legislation.

Lowering card fees is also considered a representative populist bill. Card fees were supposed to be recalculated every three years based on eligible costs (cost price) since 2007, but they have been lowered regardless during every election. In 2017, presidential candidates promised to reduce card fees, leading to further reductions and successive bill proposals. This year, with recalculation approaching, the consensus is also leaning towards lowering fees.

Populism Unleashed Under the Pretext of COVID-19

Pressure on financial companies from political circles has become more blatant since COVID-19 last year. After the crushing defeat in the April 7 by-elections, there were remarks within the ruling party blaming the Bank of Korea for not releasing enough money and commercial banks for not lending to low-income people, which led to the by-election loss. On the 28th of last month, the ruling party floor leader even brought up the idea of pardoning credit delinquents. A financial sector official expressed concern, saying, "The recent profits earned by banks were generated under the special circumstances of COVID-19, so conservative capital management is necessary to respond to uncertainties, but they are being mobilized for government and political circles' populist policies."

Concerns in the financial sector ahead of next year's presidential election are also growing. This is because populist bills and pledges aimed at winning votes have been pouring out indiscriminately from both ruling and opposition parties during every election season. During the 18th presidential election in 2012, when fierce clashes occurred between the ruling and opposition parties, then Saenuri Party candidate Park Geun-hye promised to create an 18 trillion won 'National Happiness Fund' to have financial companies purchase delinquent loans. She also promised that high-interest borrowers in their 20s and 30s would be able to switch to loans with an annual interest rate of 10% within a limit of 10 million won per person. Her opponent, then Democratic United Party candidate Moon Jae-in, proposed the so-called Pieta 3 Laws (Interest Rate Restriction Act, Fair Lending Act, Fair Debt Collection Act) to lower the interest rate ceiling in the financial sector. He also pledged to convert mortgage loans from variable interest and short-term lump-sum repayment methods to fixed interest and long-term installment repayment loans.

As the election approached, political circles tried to break down the boundaries of the private sector and pressure the government to gather votes under the role of 'collecting and adjusting public opinion,' but criticism was strong. Even during the 18th presidential election, there was criticism that private financial companies handling products were forced to provide unilateral support without any incentives, tightening the noose on financial companies. There were also voices warning that indiscriminate debtor forgiveness policies could lead to moral hazard later.

During the 19th presidential election, unrealistic financial pledges were indiscriminately made. Most candidates from both parties agreed to lower the maximum interest rate to 20%. Justice Party candidate Sim Sang-jung promised to reduce check card fees to 0% and establish a 1% cap on card fees. Democratic Party presidential candidate Lee Jae-myung proposed forgiving 5 million won per person for 4.9 million financially vulnerable people.

Government Failure Occurs When Market is Intervened... "Victims Ultimately Are Consumers"

Experts say that even considering finance as a regulated industry, government failure due to intervention can occur the moment direct manipulation beyond supervisory scope is attempted. Professor Seong Jeong-in of Hongik University’s Department of Economics pointed out, "Since finance is a regulated industry guaranteed monopoly profits, it is easier for the government to twist arms. Excessive demands lead to loans being executed where they shouldn’t be, and those who should receive loans end up not getting them, causing side effects."

Professor Sung Tae-yoon of Yonsei University’s Department of Economics criticized, "Moving finance against market principles is a significant factor that ruins the economy. Regulations are implemented to manage healthy financial movements and reduce market distortions, but ironically, government regulations are distorting the market." This means that inappropriate political intervention in the financial market is ultimately undermining market order. Professor Kim Woo-chan of Korea University’s Business School also pointed out, "The government seems to be distorting market policies too much in consideration of elections."

Professor Kim So-young of Seoul National University’s Department of Economics warned, "The current government’s market intervention is excessive and significantly ignores the original functions of finance," adding, "A kind of political risk arises for banks, making management uncertain." She criticized, "If regulations are imposed arbitrarily without clear principles, banks suffer losses and the damage may be passed on to consumers."

There were also harsh criticisms directed at financial authorities. The authorities, who should establish fair rules and foster a healthy financial industry, are said to be preoccupied with watching the populist political circles. Professor Sung Tae-yoon emphasized, "Financial authorities must act according to economic principles." Professor Seong Jeong-in also criticized, "Financial authorities themselves should reflect on moving according to political logic."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}

{kind=link}