KCCI SGI, Report on 'Evaluation and Challenges of Corporate Financial Support in Response to the COVID-19 Crisis' Released

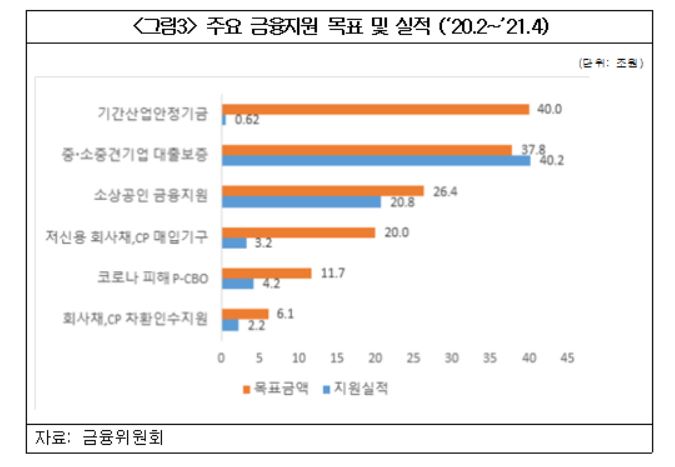

[Asia Economy Reporter Hwang Yoon-joo] Although the government’s corporate financial support measures in response to COVID-19 have contributed to alleviating market instability, the performance of major support measures remains low, prompting calls to lower the eligibility criteria and other thresholds to enhance corporate utilization. It is still too early to conclude that companies have fully emerged from the COVID crisis, and discussions on exit strategies, which have been raised by some in light of recent improvements in real economic indicators, are considered premature amid concerns over deteriorating fiscal soundness and mounting debt.

The Korea Chamber of Commerce and Industry’s SGI (Sustainable Growth Initiative) evaluated in its report titled “Evaluation and Tasks of Corporate Financial Support in Response to the COVID-19 Crisis” released on the 10th that the corporate liquidity support measures implemented to respond to COVID-19 significantly alleviated market instability. In particular, the introduction of the “Special Purpose Vehicle (SPV) for purchasing corporate bonds and commercial papers including low credit ratings” was assessed to have greatly contributed to financial market stability by conveying the government’s strong commitment to stabilization.

The report assessed that the Korean economy contracted for the first time since the foreign exchange crisis in 2020 due to the impact of COVID-19, with employment decreasing by approximately 220,000, causing a severe economic contraction and serious liquidity difficulties for companies. However, it noted that corporate financial conditions have generally improved due to government financial support measures implemented in response, and recent real economy indicators are also improving.

SGI pointed out in the report that although signs of economic recovery have recently appeared, the recovery is uneven across sectors.

In particular, for non-investment grade companies, recovery has been slow in terms of corporate bond credit spreads and net issuance volume. The credit spread, which is the interest rate difference between 3-year government bonds and corporate bonds, has continuously narrowed for investment-grade bonds (AA- rating) since the second half of last year, but recovery for non-investment grade bonds (A- rating) has been relatively slower.

Additionally, the large volume of corporate bonds maturing this year is also a burden on companies. The amount of corporate bonds maturing after March this year is 36.2 trillion KRW, which is 5 trillion KRW more than the same period last year. Maturing corporate bonds must be repaid or refinanced through new issuance, and companies facing ongoing liquidity difficulties still urgently need support to manage this smoothly. If corporate support is discontinued amid the prolonged COVID-19 situation, there is a risk of large-scale bankruptcies, which could have ripple effects on economic production and employment.

Although the government’s corporate financial support measures in response to COVID-19 have contributed to alleviating market instability, the performance of major support measures remains low, prompting calls to lower the eligibility criteria and other thresholds to enhance corporate utilization. It is still too early to conclude that companies have fully emerged from the COVID crisis, and discussions on exit strategies, which have been raised by some in light of recent improvements in real economic indicators, are considered premature amid concerns over deteriorating fiscal soundness and mounting debt.

Need to Prepare for Central Bank Interest Rate Hikes... Enhance Effectiveness of Corporate Financial Support and Respond to Industrial Structural Changes

However, concerns were also raised that the significant increase in private sector debt during the active liquidity support process could pose potential risks to the economy once monetary policy normalizes. According to the Bank of Korea, corporate debt relative to GDP in South Korea reached 110.1% in the third quarter of last year. The report also mentioned that, given the global formation of expectations for economic recovery and inflation, the timing of interest rate hikes by major central banks could be earlier than expected.

The report pointed out that for some measures with low performance relative to their targets, it is necessary to readjust eligibility criteria and the use of support funds to ensure sufficient funds are supplied where needed and to increase utilization.

The Industrial Stabilization Fund was launched with a scale of 40 trillion KRW, but as of April this year, support performance was about 600 billion KRW, only 1.5%. The low performance was attributed to strict eligibility and support conditions. The current system limits support to industries such as aviation and shipping that have experienced operational difficulties due to COVID-19, companies with total borrowings of 500 billion KRW or more, and companies with 300 or more employees. Supported companies must maintain at least 90% employment for six months.

SGI requested that the support target be expanded to include not only companies facing COVID-19 operational difficulties but also “companies seeking business restructuring and reorganization” to proactively respond to industrial structural changes after COVID-19, and that eligibility criteria such as borrowings, number of employees, and employment maintenance be relaxed.

Regarding the SPV for purchasing low credit corporate bonds and commercial papers, although it was established with a maximum of 20 trillion KRW, current purchase performance stands at only 3.2 trillion KRW. The current eligibility requires that only corporate bonds and commercial papers of companies with an interest coverage ratio of 100% or more for two consecutive years can be purchased, and the ratio of investment-grade to non-investment-grade bonds purchased is set at 25:75.

SGI requested relaxation of the interest coverage ratio requirement, noting that including 2020 in the criteria could exclude companies that temporarily suffered due to COVID-19 and raise the threshold for liquidity support for low credit companies that urgently need SPV support. According to the Financial Supervisory Service, the number of companies whose credit ratings fell last year was 54, a 22.8% increase from the previous year.

SGI also proposed expanding the proportion of non-investment-grade bonds purchased, currently set at 75%, to better align with the SPV’s purpose of supporting low credit rating companies, and extending the purchase period beyond July this year if necessary depending on market conditions.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}