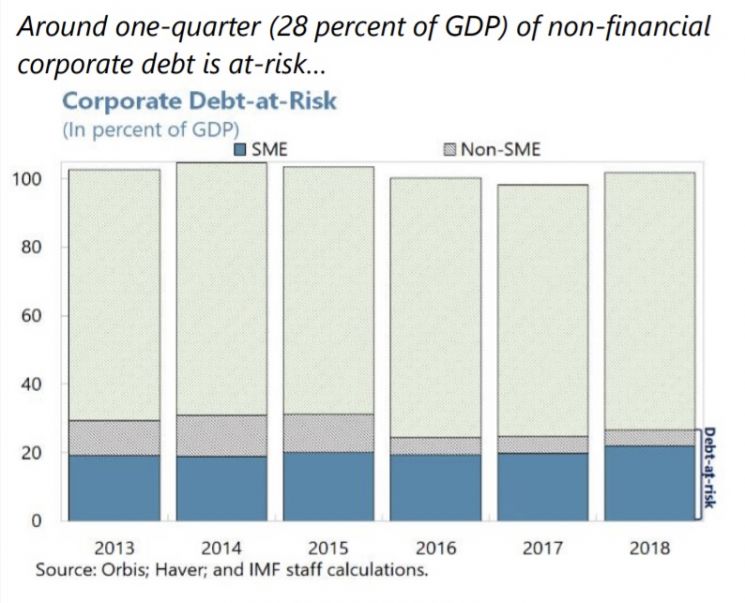

Even Without Reflecting COVID Impact, 28% Are Risky Debts

SMEs Benefit Less from Low Interest Rates Compared to Large Corporations

"Han, High SME Employment Ratio Negatively Affects Households"

Significant Portion of Risky Household Loans Concentrated in Retiree Households

[Asia Economy Reporter Kim Eun-byeol] It has been assessed that one-quarter of South Korea's corporate debt was already at a risky level even before the spread of the novel coronavirus infection (COVID-19). Most of this debt is from small and medium-sized enterprises (SMEs), with large corporate loans remaining mostly stable, while the risk associated with SME loans has increased.

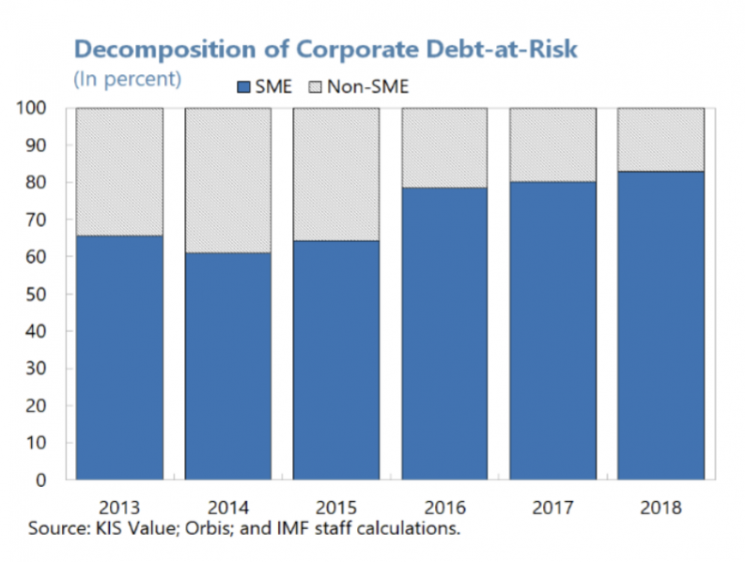

According to the 'Korea Financial Sector Assessment Program (FSAP) ? Non-Financial Balance Sheet Vulnerabilities and Financial Stability Risks' released by the International Monetary Fund (IMF) on the 18th (local time), about 28% of South Korea's non-financial corporate debt is at a risky level. Approximately 80% of the risky corporate debt is SME loans, mostly borrowed from banks. The fact that most of the high-risk loans are from SMEs is a growing concern.

The IMF interpreted, "The prolonged low-interest-rate environment has been beneficial for Korean companies, but it is also possible that the benefits of (low interest rates) were not efficiently distributed across all companies." This suggests that only large corporations may have benefited from the low-interest-rate environment. The IMF further pointed out, "Stress test results indicate that if interest rates in Korea shift to a rapid increase, the scale of corporate debt could double." Additionally, "Since SMEs account for a large share of employment in Korea, continuous instability among SMEs could eventually impact households as well," it added.

The IMF conducted the FSAP assessment last year on 12 countries including South Korea. After releasing some parts of the findings in April, it has now published a detailed report including the full evaluation results. Although the COVID-19 spread intensified during this period, the IMF clearly stated that the results do not include the impact of COVID-19.

Since 2013, more than half of the high-risk corporate loans have been loans to small and medium-sized enterprises (SMEs). In 2018, the proportion of SME loans reached approximately 80%. (Source: IMF)

Since 2013, more than half of the high-risk corporate loans have been loans to small and medium-sized enterprises (SMEs). In 2018, the proportion of SME loans reached approximately 80%. (Source: IMF)

In this report, the IMF also revealed that about 15% of South Korean household debt is at a risky level. The IMF noted, "South Korea's household leverage ratio (relative to Gross Domestic Product, GDP) is among the highest within the Organisation for Economic Co-operation and Development (OECD) countries and continues to rise," adding, "Although household loan delinquency rates are low and subprime loans are almost non-existent, the fact that more than half of bank loans are linked to variable interest rates and that the proportion of loans held by households has recently increased is problematic."

The proportion of risky loans within household debt was found to be 14%, and it was pointed out that about one-quarter of the risky household loans are held by retired households. Retirees have a high ratio of household debt relative to their income, and since most of these loans were taken out for real estate purchases, if income from real estate decreases, retirees may face difficulties in repaying their debts.

Meanwhile, the IMF assessed that even if risky debt increases according to stress test results, South Korea's financial institutions are capable of withstanding the impact. The IMF's analysis, assuming a recession scenario comparable to COVID-19, showed that only special banks affected by government policies would see a decrease in capital ratios, while savings banks, credit cooperatives, and regional banks would still meet minimum capital ratio requirements. However, the IMF highlighted the need to monitor the intensifying competition from low interest rates and fintech (financial technology), as well as the potential decline in operating profits of life and non-life insurance companies due to the aging population trend. The IMF added, "South Korea's insurance industry is saturated," and "Demographic changes place South Korea in the most disadvantageous position globally from the financial sector's perspective."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}