Removal of Provision for Lowering Reserve Rates Aligned with Banks, Insurance, and Mutual Finance Sectors

‘Provision for Bad Debt Reserve Standards’ Set Through Board Deliberation and Resolution

Establishment of Basis for Savings Banks' Own Crisis Situation Analysis System

Management Performance Evaluation Conducted When Necessary During Sector Inspections

[Asia Economy Reporter Jo Gang-wook] Financial authorities are tightening regulations on real estate project financing (PF) loans by savings banks. Accordingly, the standards for provisioning loan loss reserves related to real estate PF loans by savings banks will be significantly strengthened. To enhance crisis response capabilities, mandatory self-analysis of crisis situations will be required, and if financial authorities conduct sector inspections, management performance evaluations will also be carried out if necessary.

On the 14th, the Financial Services Commission and the Financial Supervisory Service announced that they will push forward revisions to the Mutual Savings Banks Business Supervision Regulations to enable savings banks to proactively expand their loss absorption capacity and strengthen soundness management in preparation for crisis situations.

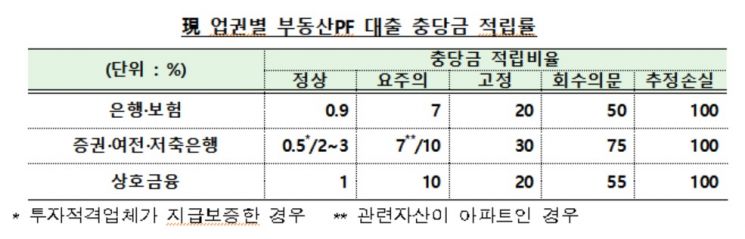

According to the proposed amendments, the provisioning standards for loan loss reserves related to real estate PF will be improved. Currently, savings banks provision loan loss reserves based on asset soundness classification for PF loans, but there were some discrepancies in the provisioning rates across different sectors. Furthermore, the criteria for lowering provisioning rates exist only in the securities, credit finance, and savings bank sectors, and there have been criticisms regarding the lack of justification for lowering these rates.

Accordingly, the provision lowering regulations were removed for savings banks, aligning them with banks, insurance, and mutual finance sectors, thereby eliminating incentives for expanding real estate PF loans by savings banks. Specifically, the regulation to lower the provisioning rate for normally classified assets when guarantees are provided by investment-grade companies (from 2% to 0.5%) was deleted, and the regulation to lower the provisioning rate for assets classified as requiring caution when the related asset is an apartment (from 10% to 7%) was also abolished.

Internal controls related to provisioning loan loss reserves will also be strengthened. It has been pointed out that many savings banks lack internal controls, such as not establishing standards or arbitrarily provisioning additional loan loss reserves beyond the minimum provisioning ratio stipulated in supervisory regulations. In particular, there is concern that arbitrary provisioning without approval from risk management committees could lead to suspicions of accounting fraud.

Provision Lowering Regulations Removed in Line with Banks, Insurance, and Mutual Finance Sectors

Financial authorities require savings banks to establish additional provisioning standards in advance and operate them consistently. These standards, including situations requiring additional provisioning and target loans, must be set through deliberation and resolution by the board of directors (or risk management committee). Additionally, savings banks are obligated to report the provisioning standards and results to the Financial Supervisory Service. However, reporting is exempted if provisioning is done according to the minimum rates stipulated in supervisory regulations. The Financial Supervisory Service will review the appropriateness of the standards and may request corrections if necessary.

A system for self-analysis of crisis situations by savings banks will be established. For large institutions with assets exceeding 1 trillion KRW, they will build their own models, while smaller institutions with assets below 1 trillion KRW will use a common standard model for savings banks. Furthermore, the Financial Supervisory Service will have the authority to request improvement plans from savings banks vulnerable to crises. This is scheduled to be implemented in January 2022, considering the revision of enforcement rules and the industry's preparation period.

Moreover, management performance evaluations can be conducted not only during comprehensive head office inspections but also during sector inspections if necessary.

Financial authorities plan to announce the legislative proposal by next month on the 26th, undergo review by the Ministry of Government Legislation and the Regulatory Reform Committee by the end of November, and finalize the resolution by the Financial Services Commission followed by notification within December this year.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}