Postponement of Interest Repayment Ends, Wave of Distressed Companies' Defaults

Growing Concerns Over Triggering Financial Crisis

[Asia Economy Reporter Kangwook Cho] The financial sector is expressing serious concerns about the extension of interest repayment deferrals for small business owners and small and medium-sized enterprises (SMEs) affected by the novel coronavirus infection (COVID-19). If they are unable to repay even the interest, these companies are essentially at the brink of collapse, making it highly likely that defaults will increase once the extension measures end. As a result, with rising delinquency rates and non-performing loan ratios, there are warnings that a 'default tsunami' could hit after the measures conclude, potentially triggering a financial crisis.

Loans with Extended Maturities and Interest Total 76 Trillion Won...Concerns Over 'Time Bomb' Loans from Insolvent Companies

According to financial authorities on the 27th, loans and interest with extended maturities across all financial sectors from February to the 14th of this month amount to a total of 76 trillion won. Of this, the outstanding balance of loans with extended maturities is 75.8 trillion won (246,000 cases), and deferred interest amounts to 107.5 billion won (9,382 cases). In particular, the five major commercial banks?KB Kookmin, Shinhan, Hana, Woori, and NH Nonghyup?have approximately 35 trillion won in loans with extended maturities and over 30 billion won in deferred interest.

The financial sector agrees with additional support measures such as extending loan maturities amid the resurgence of COVID-19. However, the problem lies with the interest repayment deferrals. Given that loan volumes have already increased significantly due to COVID-19 financial support, extending the repayment deferral once more would accumulate loan burdens during that period. This is why concerns and dissatisfaction are growing over continuing to carry the 'time bomb' loans of insolvent companies that are likely at their limit.

A senior official at Bank A said, "Extending loan maturities is an unavoidable measure, but continuously deferring interest payments inevitably becomes a significant burden for banks." He added, "Although the loans remain, the interest is not forgiven but continues to accumulate, which will lead to negative outcomes not only for financial institutions but, more importantly, for borrowers." He expressed regret, saying, "Banks have focused on extending maturities while requiring partial interest repayments and have continuously appealed this to the government, but it was not accepted."

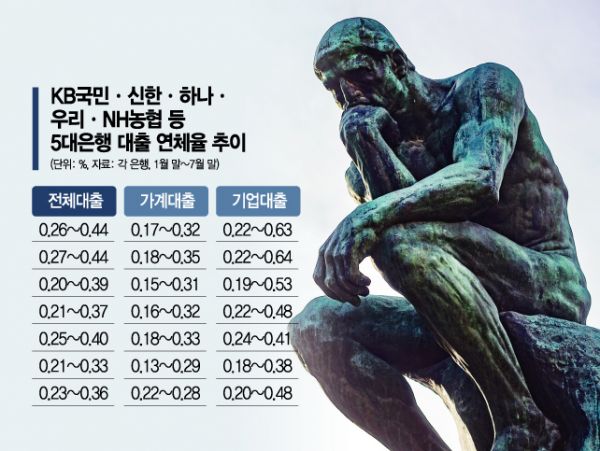

Rising Delinquent Borrowers Amid Surging Loan Demand...Household and Corporate Delinquency Rates Both Increase in July

In reality, loan demand is surging among vulnerable groups such as low-credit borrowers and small business owners, but the number of borrowers unable to repay is increasing. The household and corporate delinquency rates at the five major banks both rose in July. Corporate loan delinquency rates increased from 0.18?0.38% to 0.2?0.48%, and household loan delinquency rates also rose to 0.22?0.28% at the end of last month, showing an upward trend.

There are also criticisms that this measure merely extends the lifeline of uncompetitive insolvent companies. The more 'Evergreen Loans'?loans kept alive by borrowing more debt to repay existing debt?increase, the more the warning signals of default contagion can be distorted. Evergreen loans, where financial institutions continuously extend loan terms even though borrowers no longer have the ability to repay, are superficially classified as performing loans but are actually non-performing loans.

An official from Bank B pointed out, "It's not that interest is not being paid, but rather deferred, so defaults could worsen by February next year." He added, "Before demanding interest repayment, there should have been an opportunity to identify small companies genuinely unable to repay."

An official from Bank C also said, "It would be fortunate if normal transactions resume in the future, but companies already struggling have a high possibility of being zombie companies, which could explode all at once when the extension measures end." He emphasized, "Instead of blindly postponing, a system that allows for a soft landing is necessary."

"Just Extending the Lifeline of Insolvent Companies"...Borrowers' Credit Soundness Remains a Black Box

The situation is similar in the secondary financial sector, including credit card companies. If interest repayment is also deferred, it becomes difficult to evaluate borrowers' creditworthiness through interest payments, raising concerns that the criteria for assessing soundness will become a black box.

An official from Card Company D said, "Extending loan maturities or deferring interest repayments ultimately increases uncertainty the longer it is postponed." He added, "From the card companies' perspective, funding cost burdens inevitably increase, and it becomes harder to set aside provisions."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}