[Asia Economy Reporter Changhwan Lee] The retail distribution industry business outlook for the third quarter showed some improvement compared to the record low in the second quarter, but it still fell short of the baseline, indicating significant concerns.

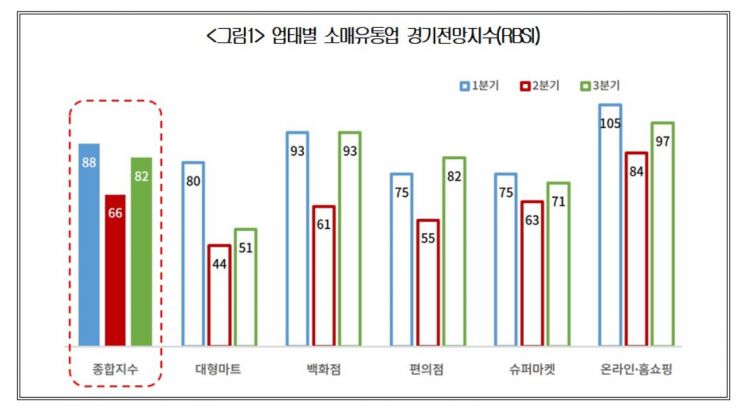

On the 5th, the Korea Chamber of Commerce and Industry announced that the ‘2020 3rd Quarter Retail Business Survey Index (RBSI)’ based on a survey of 1,000 retail distribution companies was recorded at ‘82.’

This indicates that the recession has somewhat eased compared to the record low of 66 in the second quarter, spreading positive expectations. However, all sectors still recorded below 100, suggesting that it will take time to reach a normal level. (A reading above 100 indicates an improvement outlook, below 100 indicates a worsening outlook)

The partial improvement in the 3rd quarter RBSI is attributed to a slight recovery in the previously frozen consumer sentiment. According to the Bank of Korea’s Consumer Sentiment Index, the index, which had been declining continuously since February, hit its lowest point in April and then slightly recovered from May, continuing an upward trend through June. Statistics Korea’s ‘May Retail Sales’ also increased by 4.6% compared to the previous month, and the Ministry of Trade, Industry and Energy’s ‘Major Retailers’ Sales’ showed a 2% increase year-on-year, confirming improvements in consumer sentiment and performance across various indicators.

Looking at the outlook by business type, there were differences depending on the sector. Department stores and convenience stores recorded significant increases, showing signs of emerging from the contraction in the second quarter, while large discount stores and supermarkets showed only slight increases, indicating a challenging third quarter ahead.

Department stores recorded the highest increase (32 points) among all sectors, showing strong expectations for business improvement. The department store sector experienced a deep recession with sales hitting bottom from February to April.

Recently, promotional events such as the ‘Companion Sale’ and ‘Domestic Sales of Duty-Free Goods’ succeeded in reversing sales, and this positive momentum is expected to continue for some time. In particular, with the start of summer vacations, improvements in sales of fashion accessories such as clothing and cosmetics have been observed, supporting the positive outlook.

Convenience stores also recorded a large increase (27 points) driven by sales growth and seasonal effects. Although they showed the second-highest negative outlook (55) last quarter, sales increased due to disaster relief fund usage, and the allowance of mobile alcohol (wine) sales (from April) emerged as a new revenue source, raising expectations for business improvement. Additionally, summer is considered the peak season for convenience stores due to increased beverage sales in hot weather and more late-night activities, leading to a positive outlook.

Large discount stores recorded the lowest outlook (44) last quarter due to a sharp decline in visitors and losing even food and daily necessities, which account for most of their sales, to online channels. They were also excluded from disaster relief fund usage in the second quarter, missing out on sales stimulation effects. The recovery outlook for the third quarter remains bleak. Restrictions such as operating hour limits and mandatory closures have weakened competitiveness, and it is considered difficult to bring back consumers who have stopped visiting due to COVID-19, negatively impacting the outlook (51).

Supermarkets showed only a slight increase (8 points) to an outlook of 71, with no clear performance improvement expected in the third quarter. Supermarkets benefited from their proximity to residential areas during the large-scale COVID-19 outbreak. However, the period of this benefit was short as consumers shifted to online purchasing through same-day fresh food delivery services, and intense competition among companies negatively affected sales.

Online and home shopping recorded the highest outlook (97) among all sectors. Last quarter, online sales fell below 100 for the first time in 10 years due to sluggish sales of items other than daily necessities. Although the third quarter outlook remains negative,

recent recovery in consumer sentiment has increased sales of household and furniture items, and the ‘Top Efficiency Home Appliance Purchase Cost Rebate Program’ has boosted home appliance sales, supporting performance improvement. Industry insiders expect that if there is no resurgence of COVID-19, the outlook will continue to improve and soon recover to previous levels.

Looking at the trends in domestic retail distribution industry outlook during past epidemic outbreaks, SARS (’02) and H1N1 flu (’09) showed a rebound (above 100) in the second quarter after hitting their lowest points. In contrast, MERS failed to rebound after the drop and remained in a trend of negative outlooks.

In the case of MERS, the high fatality rate (35%) caused anxiety to have a much greater impact compared to the previous two cases, making it difficult for consumer sentiment to recover. On the other hand, although the number of domestic H1N1 infections (760,000) was very high, the relatively low mortality rate limited anxiety.

COVID-19 caused unprecedented contraction in consumer sentiment due to its rapid spread, and local infections and asymptomatic cases continue to act as sources of uncertainty in economic activities. The third quarter outlook predicts some easing of the recession, but the Chamber of Commerce emphasized that a strong consumer activation in this quarter is necessary to create a turning point and expect a rebound in the fourth quarter.

Kang Seok-gu, head of the Industrial Policy Team at the Korea Chamber of Commerce and Industry, said, “Although positive effects such as improved consumer sentiment and resulting performance have partially appeared due to government measures to stimulate domestic demand, it is still difficult to say that the situation has returned to normal. To maintain the recovery trend, additional timely government economic reinforcement policies are needed, and reasonable improvements in distribution regulations must follow to give momentum to consumer recovery.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}