If COVID-19 Prolongs, More Companies Will Become Distressed... Moody's Also Issues Warning

[Asia Economy reporters Kangwook Cho and Haeyoung Kwon] As the spread of the novel coronavirus infection (COVID-19) has dealt a blow to small and medium-sized enterprises (SMEs) and self-employed individuals, the banking sector is facing an emergency in managing asset soundness. Commercial banks have continuously increased loans to SMEs and the self-employed over the past few years and are currently expanding financial support such as interest rate reductions and new funding supply for SMEs and small business owners in response to COVID-19. Accordingly, concerns are growing that if the COVID-19 crisis prolongs, a surge in marginal companies will occur, worsening the asset soundness of banks.

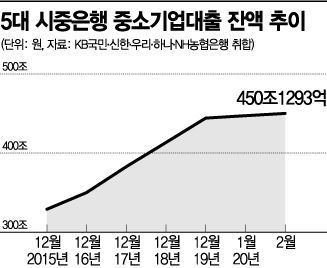

According to the financial sector on the 9th, the outstanding SME loans (including individual business owners) of the five major commercial banks?Shinhan, KB Kookmin, Woori, Hana, and NH Nonghyup?as of the end of February amounted to 450.1293 trillion KRW, an increase of 2.8818 trillion KRW compared to the previous month (447.2475 trillion KRW). Excluding individual business owners, the outstanding SME loan balance increased by 1.3293 trillion KRW from 206.8686 trillion KRW to 208.1979 trillion KRW during the same period.

Banks have increased financial support for these companies in line with the government’s SME and venture business promotion policies over recent years. In fact, the outstanding SME loan balance of the five major commercial banks rose from 329.0653 trillion KRW in 2015 to 444.2247 trillion KRW last year, an increase of 115.1594 trillion KRW over four years, averaging about 28.8 trillion KRW annually.

However, looking at the recent growth scale, there is a forecast that the upward curve of SME loans in the banking sector will be steeper this year. The increase in January alone was 3.0228 trillion KRW, and from January to February, it was 2.8818 trillion KRW, totaling 5.9046 trillion KRW over two months. Arithmetically, this suggests that SME loans could increase by 35.4276 trillion KRW over the entire year. This figure exceeds last year’s increase by about 5 trillion KRW and surpasses the average annual figure over the past four years by 6.6 trillion KRW. Amid this, banks have decided to expand the scale of new special loan funds by 1.4 trillion KRW compared to previous levels.

The problem is that if COVID-19 prolongs, the risk of SME loan defaults will increase, potentially causing liquidity shortages in the banking sector. Economic sentiment has frozen, and industries directly hit such as low-cost carriers (LCCs) and the travel sector are expected to see a surge in marginal companies. The financial investment industry estimates the total risk exposure of banks to three sectors?LCC airlines (220.7 billion KRW), travel (51.3 billion KRW), and film (182.7 billion KRW)?to be about 454.7 billion KRW.

The situation is even more severe for regional banks. DGB Financial and BNK Financial have a high proportion of SME loans, accounting for 60-70% of total credit, and the share of self-employed (SOHO) loans also exceeds 20% of total credit, which is higher than other banks.

Currently, SMEs in the Daegu and Gyeongbuk regions have halted factory operations, and self-employed business activity has completely stagnated due to avoidance of outings amid infection concerns. According to the Bank of Korea, the Consumer Sentiment Index (CIS), a current economic indicator, plummeted from 70 in January to 57 in February in the Daegu and Gyeongbuk regions. This is the largest drop since the MERS (Middle East Respiratory Syndrome) outbreak in May 2015, when the index fell from 81 in May to 66 in June.

The collapse of existing core industries remains a risk factor for regional banks. According to the Korea Deposit Insurance Corporation, as of the end of September 2019, the proportion of loans related to the top four industries with signs of distress estimated by the Financial Supervisory Service?machinery equipment, real estate, auto parts, and metal processing?accounted for 26.9% of total loans by regional banks. This is about 10 percentage points higher than the 17% for commercial banks.

International credit rating agency Moody’s has also raised warnings. In a recent report, Moody’s expressed concern that "the spread of COVID-19 may cause disruptions in many domestic industries, which could lead to an expansion of asset soundness risks for some banks exposed to these impacts."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}