Continued Low Interest Rates Lead to Profitability Decline

Interest-Linked Debt Increases by 6%

[Asia Economy Reporter Oh Hyung-gil] Even as interest rates fall, the scale of interest rate risk arising from the minimum guaranteed interest rate promised to policyholders has exceeded 200 trillion won among the 'Big 3' life insurance companies. Although life insurers significantly reduced high-interest savings products, which were cited as the main cause of negative spreads in last year's low-interest-rate environment, the minimum guaranteed interest rate, which exceeds the operating asset yield, still remains at a considerable level.

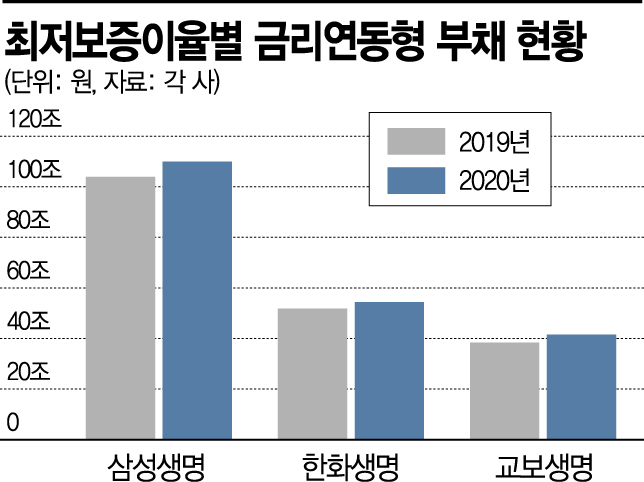

According to the insurance industry on the 5th, the scale of interest rate-linked liabilities by minimum guaranteed interest rate for the three companies?Samsung, Hanwha, and Kyobo Life Insurance?stood at 205.78 trillion won as of the end of last year. This represents a 6.0% increase from 194.07 trillion won the previous year.

Samsung Life Insurance's interest rate-linked liabilities increased by 5.7% from 103.94 trillion won in 2019 to 109.93 trillion won last year. By interest rate bracket, liabilities with guaranteed interest rates in the 'over 0% up to 2%' range surged by 14.3% to 49.25 trillion won compared to the previous year, while the 'over 3% up to 4%' bracket grew by 3.2%, and the 'over 4%' bracket expanded by 2.8%.

During the same period, Hanwha Life Insurance grew by 4.9% to 54.36 trillion won. Liabilities in the bracket exceeding 3% alone amounted to 13.50 trillion won, a 1.3% increase from the previous year. Kyobo Life Insurance also saw a sharp rise of 8.2%, from 38.33 trillion won to 41.50 trillion won.

Interest rate-linked insurance products set a minimum guaranteed interest rate to ensure policyholders receive at least the death benefit and surrender value, even when market interest rates fall. The higher rate between the applied rate (disclosed interest rate) and the minimum guaranteed interest rate is applied and returned to the policyholder.

Although the disclosed interest rate is being lowered to manage interest rate-linked liabilities, if minimum guaranteed liabilities continue to increase, it inevitably negatively impacts profitability. Past high-interest-rate products sold can act as a factor that increases the risk of negative spreads in a low-interest-rate environment.

In particular, last year, due to the prolonged ultra-low interest rates caused by COVID-19, savings-type insurance products experienced an unusual boom, amplifying the impact of interest rates. According to last year's life insurance premium income data, savings-type insurance increased nearly twice as much as protection-type insurance, which rose by 3.105 trillion won compared to the previous year.

To secure returns above the minimum guaranteed interest rate, asset management yields must be raised, but life insurers' operating asset yields remain at low levels.

Last year, Samsung Life Insurance's operating asset yield was 3.2%, down 0.2 percentage points from the previous year. Hanwha Life Insurance maintained 3.5%, but Kyobo Life Insurance fell from 3.9% to 3.7%.

From 2023, under the new international accounting standards (IFRS17) and the new solvency regime (K-ICS), insurance liabilities must be evaluated at market value, and cash flows related to the minimum guaranteed interest rate must be assessed to set aside reserves.

Ultimately, life insurers are responding by lowering the minimum guaranteed interest rate, but there are concerns that this could also lead to premium increases. A life insurer official said, "We are preparing interest rate response measures, such as reflecting asset management performance in the guaranteed interest rates of new products," adding, "With recent increases in market interest rates, the burden of interest rate risk is expected to ease somewhat."

Researcher Noh Geon-yeop of the Korea Insurance Research Institute advised, "Regarding the minimum guaranteed interest rate, it is necessary to set it reasonably considering the long-term declining trend of interest rates and the characteristics of long-term maturity products. Asset management yields should be improved to secure returns above the minimum guaranteed interest rate, and by linking asset management performance with the guarantee levels of new products and adjusting accordingly, the burden of guarantee reserves should be managed within asset management performance."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}

{kind=link}